Warren Buffett and the Power of Compounding: How Wealth Is Really Built

- Alpesh Patel

- Jan 6

- 5 min read

What Multi-Decade Conviction Teaches Everyday Investors About Real Wealth Creation

Long-term investing is easy to admire and extraordinarily hard to practice.

Everyone celebrates it in hindsight. Very few survive it in real time.

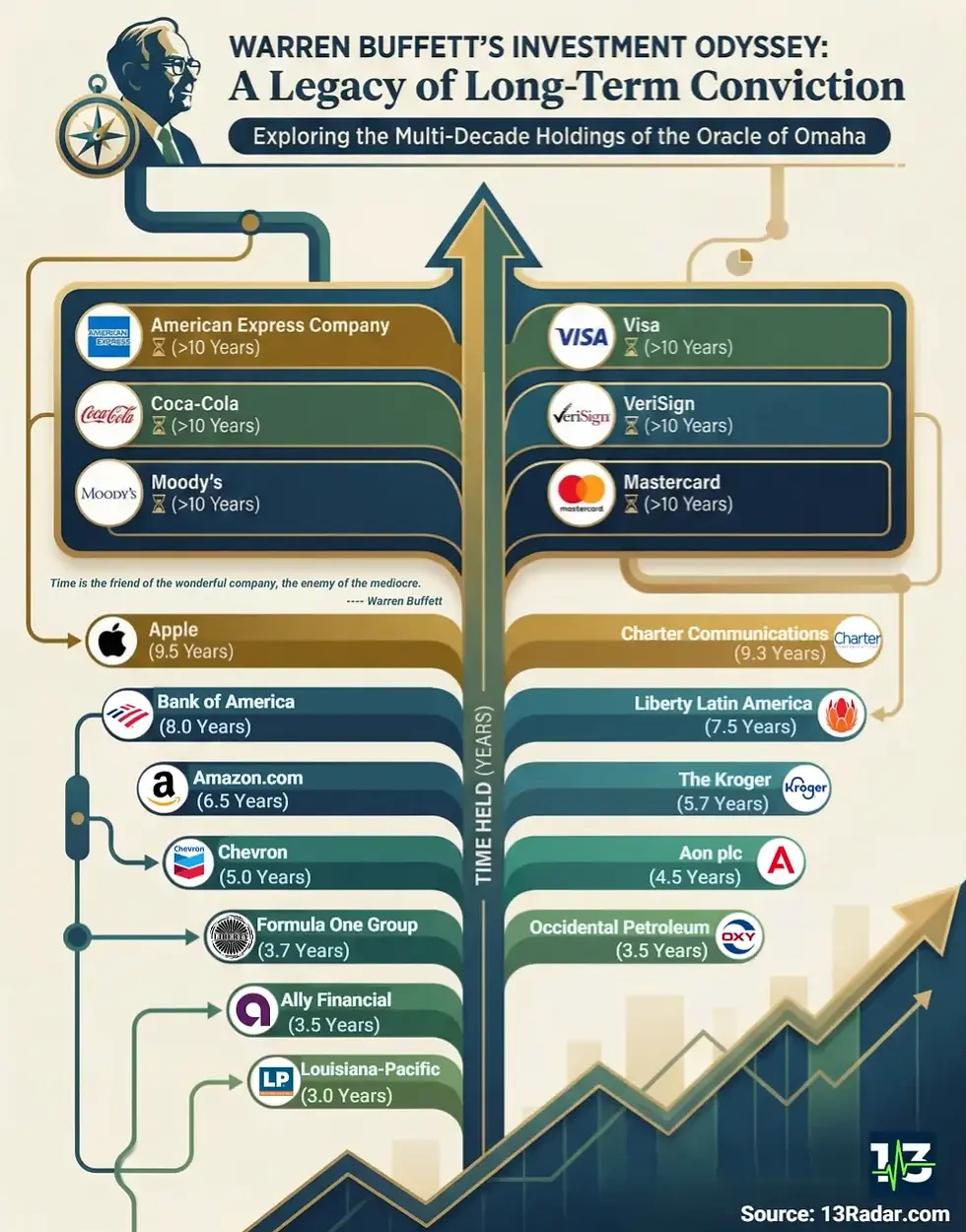

The image above – mapping multi-decade holdings associated with Warren Buffett’s investment career – is not just a visual history lesson. It is a psychological stress test.

It shows what it actually takes to build extraordinary wealth: patience measured in years, not quarters; conviction grounded in business fundamentals, not narratives; and the emotional discipline to do nothing while others panic.

This image reinforces a central truth:

Wealth is rarely created by brilliance.It is created by behaviour.

This article unpacks what this visual really teaches and why these lessons matter far more for everyday investors than copying individual stocks ever could.

Why This Image Matters More Than Any “Top 10 Stocks” List

At first glance, the image appears simple: a list of well-known companies held for long periods. But simplicity is deceptive.

This is not a story about genius stock selection. It is a story about time arbitrage, the ability to think in decades while most of the market is trapped in months.

The visual highlights something uncomfortable:

Most returns were not made in the first year

Many positions looked “boring” or “fully valued” for long stretches

Several holdings went through severe drawdowns before delivering exceptional long-term results

This is exactly why the Great Investments Programme consistently emphasises process over prediction.

Warren Buffett and the Myth of Constant Activity

The dominant myth in investing is that success requires action.

Trade more. React faster. Adjust constantly.

The reality, demonstrated repeatedly throughout Warren Buffett’s career, is the opposite.

Buffett’s edge was never speed. It was inactivity backed by conviction.

He understood something most investors struggle with:

Compounding does not reward intelligence.It rewards endurance.

Understanding the Core Message

The image categorises holdings by time held, not by returns.

That distinction matters.

Time held is the silent driver of wealth. Returns are merely the outcome.

Across the visual, you’ll notice three broad categories:

1. Multi-Decade Anchors (>10 years)

2. Long-Term Compounders (5–10 years)

3. Shorter-Cycle Convictions (3–5 years)

Each category reflects a different role within a disciplined portfolio framework.

This mirrors the portfolio layering approach taught inside the Great Investments Programme where assets serve specific purposes rather than chasing short-term excitement.

The Power of Multi-Decade Holdings

American Express, Coca-Cola, Moody’s, Visa, Mastercard, VeriSign

These companies share common traits:

Strong pricing power

Durable competitive advantages

Predictable cash flows

Structural tailwinds

Simple business models

None of them required constant monitoring.

None depended on perfect timing.

All benefited from time.

This is why the Campaign for a Million consistently pushes back against the obsession with “the next big thing”. The next big thing rarely stays big. Enduring businesses do.

Time Is the Only Unfair Advantage Retail Investors Have

Institutional investors are constrained.

Performance reporting

Career risk

Client impatience

Quarterly benchmarks

Individual investors have none of these constraints, if they choose not to.

This is one of the central teachings of Alpesh Patel’s educational work:

The biggest edge most investors waste is patience.

The image makes this visible.

Holding something for 10, 15, or 20 years is not glamorous but it is extraordinarily powerful.

Apple: A Case Study in Behavioural Fortitude

One of the most discussed holdings in the image is Apple.

What is often forgotten:

Apple spent years going nowhere

It suffered multiple sharp drawdowns

It was repeatedly declared “too big to grow”

Yet patient capital was rewarded.

Not because Apple was perfectly timed; but because the holding period allowed compounding to work.

This reinforces a key principle:

You do not need perfect decisions.You need decisions that you can stick with.

Bank of America, Amazon, Chevron: Riding Through Cycles

Cyclicality Is Not Risk, Behaviour Is

Many investors confuse volatility with danger.

But volatility is normal. Panic is optional.

Companies like Bank of America, Amazon, and Chevron all experienced:

Macro shocks

Sector rotations

Regulatory fears

Media negativity

This quietly reminds us: the investor who endured these phases captured the compounding. The one who reacted emotionally did not.

Why “Doing Nothing” Is the Hardest Skill in Investing

In the Great Investments Programme, one of the most uncomfortable lessons is this:

The most profitable action is often inaction.

Doing nothing feels irresponsible.

It feels lazy.

It feels wrong, especially when markets are volatile.

But the image shows that strategic inaction is not passive. It is a deliberate, disciplined choice.

The Role of Shorter-Term Holdings

Not every holding lasted decades.

That matters too.

Companies held for 3–5 years often served specific portfolio roles:

Tactical exposure

Cyclical opportunities

Temporary valuation mismatches

This is where process discipline matters most.

Shorter holdings are not failures provided they are exited for the right reasons, not emotional ones.

What the Image Does Not Say (And Why That Matters)

This visual is often misunderstood.

It does not say:

Buy these stocks now

Copy this portfolio

Ignore valuation

Never sell anything

Those conclusions miss the point entirely.

The image teaches behavioural discipline, not stock selection.

That distinction is central to Alpesh Patel’s educational framework.

The Psychological Cost of Compounding

Compounding is mathematically simple.

Psychologically, it is brutal.

To benefit from compounding, investors must tolerate:

Long periods of boredom

Extended underperformance vs headlines

Criticism from peers

Self-doubt during drawdowns

The image compresses decades of emotional stress into a neat diagram, but living through it is far messier.

This is why Campaign for a Million focuses so heavily on investor mindset, not just numbers.

Why Most Investors Never Experience True Compounding

Most investors interrupt compounding before it has a chance to work.

They:

Switch strategies

Chase performance

React to headlines

Over-monitor portfolios

The image demonstrates the opposite approach:

Decide carefully

Allocate sensibly

Hold patiently

Review rationally

Portfolio Construction vs Stock Worship

One of the most dangerous behaviours in investing is hero worship.

The goal is not to be Warren Buffett.

The goal is to build a repeatable, disciplined process that works for your life, temperament, and time horizon.

This is exactly why the Great Investments Programme teaches portfolio thinking, not stock tips.

How This Image Aligns with Campaign for a Million

Campaign for a Million is not about shortcuts.

It is about helping investors:

Avoid catastrophic mistakes

Reduce unnecessary costs

Let compounding work over time

Stay invested through cycles

This image is a visual summary of that philosophy.

It shows what happens when:

Behaviour is controlled

Time is respected

Emotions are managed

Decisions are evidence-based

The Unfashionable Truth About Wealth

Wealth is not built by:

Constant optimisation

Endless tweaking

Emotional reactions

It is built by:

Sound decisions

Adequate diversification

Long time horizons

Staying invested

The image captures this better than any spreadsheet ever could.

Why This Matters More in 2026 and Beyond

Markets today are noisier than ever.

Social media amplifies fear

News cycles reward panic

Algorithms reward outrage

In this environment, long-term conviction becomes even more valuable — and rarer.

This is why Alpesh Patel consistently reminds investors:

The future belongs to those who can ignore most of the present.

Final Reflection: The Quiet Power of Time

The most important takeaway from the image is not which companies appear on it.

It is the timeline.

Time is the common denominator behind every successful outcome.

If there is one lesson investors should internalise from this visual, it is this:

Compounding is not a formula.It is a test of character.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Investing involves risk, including the loss of capital. Readers should conduct their own research or consult a qualified financial professional before making investment decisions.

Alpesh Patel OBE

Comments