Nest Pension Review 2026: Is the UK's Biggest Auto-Enrolment Scheme Working for You?

- Alpesh Patel

- Mar 26

- 6 min read

Updated: Apr 9

Nest is the most widely held pension scheme in UK history. And most of its 12 million members have never looked at what it actually does with their money.

The National Employment Savings Trust was created by the UK government in 2010 as the default pension provider for auto-enrolment. Its explicit purpose was to serve workers who had no other pension provision — particularly those in lower-paid employment and smaller businesses where no employer scheme existed. It was never designed as the ideal pension vehicle for an analytically capable professional who is actively managing their own wealth.

In the GIP portfolio reviews I conduct with clients, Nest pots appear with some regularity — usually from a previous employer, often from the early years of a career, and almost always unreviewed. The question every time is the same: is this the right home for that money, or should it be consolidated into a self-directed SIPP where it can work harder?

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. Through the Great Investments Programme he reviews pension fund holdings for UK investors, and Nest pots are a recurring part of that work.

What Nest Is and How It Works

Nest is a public corporation established by the UK government under the Pensions Act 2008. It operates as a defined contribution pension scheme with a trustee board and is regulated by the Pensions Regulator. As at 2026, it has over 12 million members and manages over £40 billion in assets, making it one of the largest DC schemes in the country by member count.

Most members are invested in Nest’s default fund: the Nest Retirement Date Fund. This is a target-date fund that selects the fund with the closest retirement date to the member’s 65th birthday.

The fund automatically adjusts its asset allocation over time, starting with higher equity exposure in the ‘foundation phase’ and ‘growth phase’ decades, and shifting toward bonds and cash in the ‘consolidation phase’ in the final years before the target retirement date.

Nest Charges: The Contribution Fee Problem

Nest’s charging structure has two components that every member should understand:

Annual management charge (AMC): 0.3% per year on the total value of your pot. This is competitive — lower than most managed pension funds and broadly in line with many low-cost index trackers.

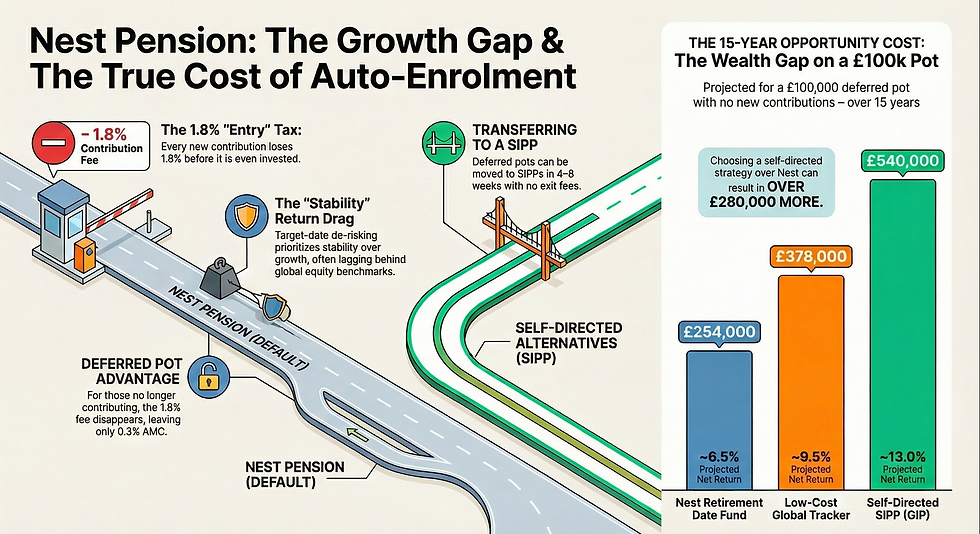

Contribution charge: 1.8% on each new contribution made to the scheme. This is deducted from every payment going in before it is invested.

The 1.8% contribution charge is the distinctive and often under-appreciated cost of Nest. For every £100 paid into Nest, only £98.20 is invested. This does not sound alarming in isolation. But consider an investor contributing £1,000 per month: £18 of every contribution is consumed by the contribution charge before a single penny is invested. Over a full year of £1,000/month contributions, the contribution charge costs £216 — on top of the 0.3% AMC.

For members who are no longer contributing to their Nest pot — because they have left the employer who enrolled them — the contribution charge is irrelevant. Only the 0.3% AMC applies to the existing pot. In this scenario, Nest’s charges are actually competitive.

Nest Fund Performance: What the Data Shows

Nest’s Retirement Date Funds have delivered returns broadly in line with a diversified multi-asset portfolio at their respective equity weightings.

The 2040 Retirement Date Fund the closest to a long-term growth vehicle for mid-career members has historically returned approximately 7–8% per year gross over 5-year periods, with net returns of approximately 6.5–7.5% after the 0.3% AMC.

This is not dramatically different from other managed multi-asset pension default funds. The same structural limitations apply: a meaningful allocation to bonds and other non-equity assets during the growth phase dilutes returns relative to a pure global equity tracker, and the target-date de-risking mechanism reduces equity exposure significantly in the final decade before retirement.

Against the MSCI World Total Return Index (GBP), which returned approximately 12% per year over the decade to 2024, the Nest default fund has lagged significantly. This gap typical of multi-asset pension default funds across the UK industry is the structural return drag from bonds, diversified alternatives, and systematic de-risking that prioritises stability over growth.

The 15-Year Gap: Three Scenarios on a £100,000 Nest Pot

Take a deferred £100,000 Nest pot (no further contributions) with 15 years to retirement:

Nest Retirement Date Fund (~6.5% net): grows to approximately £254,000

Low-cost global equity tracker (9.5% net): grows to approximately £378,000

GIP self-directed SIPP (13% net): grows to approximately £540,000

Transferring a £100,000 Nest pot to a self-directed SIPP and applying the GIP framework produces approximately £286,000 more over 15 years compared to leaving it in Nest’s default fund. Run your own numbers at campaignforamillion.com/tools.

When Leaving Your Money in Nest Makes Sense

Nest’s default fund is not without merit in specific circumstances. For investors who are not willing or able to manage a self-directed SIPP, Nest provides a low-admin, regulated, multi-asset pension with competitive AMC charges. For very small pots where the administrative overhead of a SIPP transfer outweighs the benefit, leaving a Nest pot in place until a meaningful balance has accumulated may be pragmatic. And for active contributors who value simplicity above return optimisation, Nest’s structure is functional if not optimal.

But for analytically capable investors who are already managing a SIPP or ISA portfolio — the GIP audience — a deferred Nest pot above £25,000–30,000 is almost always better consolidated and redeployed under a systematic quantitative framework.

Frequently Asked Questions: Nest Pension

Is Nest a good pension?

Nest is a legitimate, regulated, government-backed pension with competitive AMC charges (0.3%) and a functional multi-asset default fund. For its original purpose — providing a default pension for workers with no other provision — it works adequately. For an engaged, analytically capable investor who wants to maximise long-run returns and has a self-directed SIPP or ISA portfolio, it is not the optimal vehicle.

What are Nest pension charges?

Nest charges 0.3% annual management charge on the total pot value, plus a 1.8% contribution charge on each new contribution going in. The contribution charge is the more unusual element — most other pension providers charge only an AMC. For deferred members (no longer contributing), only the 0.3% AMC applies.

Can I transfer my Nest pension to a SIPP?

Yes. Deferred Nest pots (where you are no longer actively contributing through an employer) can be transferred to a self-directed SIPP. Nest does not charge an exit fee for transfers. The process takes 4–8 weeks and is managed by the receiving SIPP provider. You cannot transfer a Nest pot if you are still an active member contributing through your current employer.

What is the Nest Retirement Date Fund?

The Nest Retirement Date Fund is Nest’s default investment. It selects the target-date fund closest to your 65th birthday and automatically adjusts asset allocation over your working life — higher equity exposure in earlier decades, shifting progressively toward bonds and cash as retirement approaches. Like all lifestyle/target-date strategies, the de-risking mechanism reduces growth potential in the final decade when the pot is at its largest.

How do I find my old Nest pension?

If you were auto-enrolled into Nest by a previous employer, you can log in or register at nest.co.uk using your National Insurance number. Nest will hold your pot indefinitely as a deferred member. If you are unsure whether you have a Nest pot, the government’s free Pension Tracing Service at gov.uk/find-pension-contact-details can identify pension providers for previous employers.

If you hold a Nest pot and want to understand what it is worth and what the alternatives look like, run your numbers at campaignforamillion.com/tools. For a full review of your Nest pot alongside your other pension holdings, book a free portfolio review here.

Sources & Further Reading

Nest Corporation — Annual Report and Accounts 2025. Scheme size, member numbers, and fund performance data. nestpensions.org.uk

The Pensions Regulator — Auto-enrolment guidance and workplace pension governance standards. thepensionsregulator.gov.uk

Financial Times — Auto-enrolment pension performance reviews and Nest coverage. ft.com/personal-finance

Yodelar — Independent UK pension fund performance rankings including Nest. yodelar.com

PLSA — Retirement Living Standards (2024). Comfortable retirement income benchmarks. plsa.co.uk

MSCI — MSCI World Total Return Index (GBP). Benchmark for global equity returns. msci.com/world

Gov.uk — Pension Tracing Service. Find contact details for previous employer pension schemes. gov.uk/find-pension-contact-details

Disclaimer: This article is for educational purposes only. Performance projections are illustrative. This does not constitute personal financial guidance. All investing carries risk. Past performance is not a reliable indicator of future results.

Alpesh Patel OBE

Comments