Scottish Widows CS8 Pension Portfolios Reviewed: Why All Five Underdeliver

- Alpesh Patel

- Mar 23

- 4 min read

Updated: Mar 25

Most people in a Scottish Widows workplace pension have no idea which fund they are in.

If you were auto-enrolled into a Scottish Widows workplace pension, you were most likely defaulted into one of their Pension Portfolio funds — labelled Portfolio One through Five, with the CS8 suffix indicating their structure within the scheme. Your portfolio number reflects the risk category assigned to you based on your age and years to retirement.

The question this post answers: does the fund you are in — whichever one it is — actually serve your retirement interests? The answer, across all five portfolios, is the same.

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. His earlier review of Scottish Widows Pension Portfolio Two (CS8) is one of the most-read posts on campaignforamillion.com.

How the Scottish Widows CS8 Portfolio Range Works

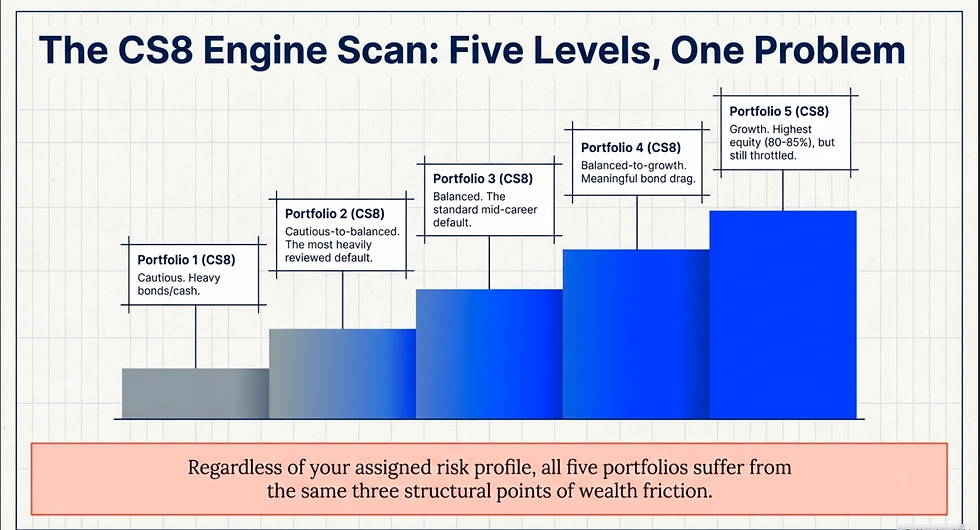

The five Pension Portfolio CS8 funds represent a risk ladder from cautious to adventurous. Each holds a different blend of equities, bonds, property, and cash:

Portfolio One (CS8): Cautious. Predominantly bonds and cash, minimal equity. Designed for those close to or at retirement.

Portfolio Two (CS8): Cautious-to-balanced. Majority bonds with some equity. The subject of our earlier in-depth review.

Portfolio Three (CS8): Balanced. Roughly equal split between equities and bonds. The most common default for mid-career savers.

Portfolio Four (CS8): Balanced-to-growth. Majority equities with meaningful bond exposure.

Portfolio Five (CS8): Growth. The highest-equity option in the range, typically 80–85% equities.

As you approach retirement, Scottish Widows’ lifestyling mechanism automatically moves your holding down the range — from Portfolio Five toward Portfolio One and Two — reducing equity exposure and increasing bonds and cash. This is designed to ‘protect’ your pot near retirement.

The Problem That All Five Portfolios Share

Every portfolio in the CS8 range has the same three structural problems, regardless of its risk rating.

1. Fees That Compound Against You

Independent analysis of over 645 Scottish Widows pension funds found that 50% consistently underperformed their sector average — and that is before accounting for the fee disadvantage. Total charges across the CS8 range typically run to 0.60–1.0% per year. A low-cost passive alternative runs 0.07–0.22%. That 0.4–0.8% annual gap compounds silently over 20–30 years into tens or hundreds of thousands of pounds.

2. Bond Drag Across the Range

Even Portfolio Five — the ‘growth’ option — holds 15–20% in non-equity assets. During the 2010s equity bull market and the post-2020 recovery, these allocations dragged significantly below the equity market return. Portfolios One through Three, with their heavy bond weighting, have delivered sub-inflation returns in real terms during multiple extended periods.

3. Lifestyling Destroys Growth at the Worst Time

The automatic lifestyling mechanism — moving savers from Portfolio Five toward Portfolio One as they approach retirement — reduces equity exposure during the years when the pot is at its largest. A 55-year-old being moved from Portfolio Four to Portfolio Two is having their growth engine throttled at exactly the point in their investing life when each percentage point of return has the greatest absolute impact on their final pot.

Portfolio by Portfolio: What the Numbers Show

The following comparison uses a £100,000 pot over 20 years to illustrate the performance gap for each portfolio vs a 100% global equity index tracker at 9.5% net:

Portfolio One (~3% net): £181,000 — barely ahead of inflation. Gap vs tracker: £432,000

Portfolio Two (~4.5% net): £241,000. Gap vs tracker: £372,000

Portfolio Three (~5.5% net): £292,000. Gap vs tracker: £321,000

Portfolio Four (~6.5% net): £352,000. Gap vs tracker: £261,000

Portfolio Five (~7.5% net): £424,000. Gap vs tracker: £189,000

Global equity tracker (9.5% net): £613,000

Even Portfolio Five — the best of the five — trails a simple tracker by £189,000 over 20 years on a £100,000 pot. Portfolio One trails by £432,000. These are not rounding errors. They are the compounded cost of 20 years of fee drag and sub-optimal allocation.

Frequently Asked Questions: Scottish Widows CS8 Portfolios

Which Scottish Widows CS8 portfolio is best?

Portfolio Five delivers the highest expected return due to its greater equity weighting, and is the strongest performer over long time periods. But even Portfolio Five trails a low-cost global equity tracker significantly over 10–20 years. The right question is not which CS8 portfolio is best — it is whether any of them is the best option for your retirement.

Is Scottish Widows Pension Portfolio Five (CS8) a good investment?

Portfolio Five has a higher equity allocation than lower-numbered portfolios and has delivered the best returns within the CS8 range. However, it still carries charges that compound against you and holds 15–20% in non-equity assets. Over 20 years, the gap between Portfolio Five and a low-cost global equity tracker is approximately £189,000 on a £100,000 starting pot.

Why does Scottish Widows move me to a lower portfolio as I approach retirement?

This is called lifestyling — an automatic process that reduces equity exposure as you approach your target retirement date. The theory is that it reduces volatility risk. The practical effect is that it dramatically reduces your growth rate during the years when your pot is largest. A self-directed investor can make this choice consciously, based on their actual situation, rather than having it applied automatically.

Can I switch out of my Scottish Widows CS8 pension?

Yes. Scottish Widows workplace pensions are typically defined contribution schemes with no exit penalty, and can be transferred to a self-directed SIPP with a provider such as Hargreaves Lansdown, AJ Bell, or Interactive Investor. The process takes 4–8 weeks and is managed by your new provider. Always confirm there are no guaranteed benefits or final salary links before transferring.

What is the Scottish Widows CS8 Portfolio Two review?

Our detailed review of Portfolio Two — the most widely held default in the CS8 range for mid-career savers — is available at The Pension Trap: Why Scottish Widows Portfolio Two (CS8) Holds You Back.

If you are in any Scottish Widows CS8 portfolio and want to understand what the performance gap means for your retirement, book a free pension review at campaignforamillion.com. Alpesh’s team will run your current fund through the numbers and show you the gap.

Disclaimer: This article is for educational purposes only. Performance projections are illustrative and based on estimated net returns. All investing carries risk. Past performance is not a reliable indicator of future results. This does not constitute personal financial guidance.

Alpesh Patel OBE

Comments