The 4% Rule Explained: How Much Do You Really Need to Retire in the UK?

- Alpesh Patel

- Mar 23

- 5 min read

Updated: Mar 25

In 1998, three finance professors at Trinity University in Texas published a paper that quietly changed how the world thinks about retirement.

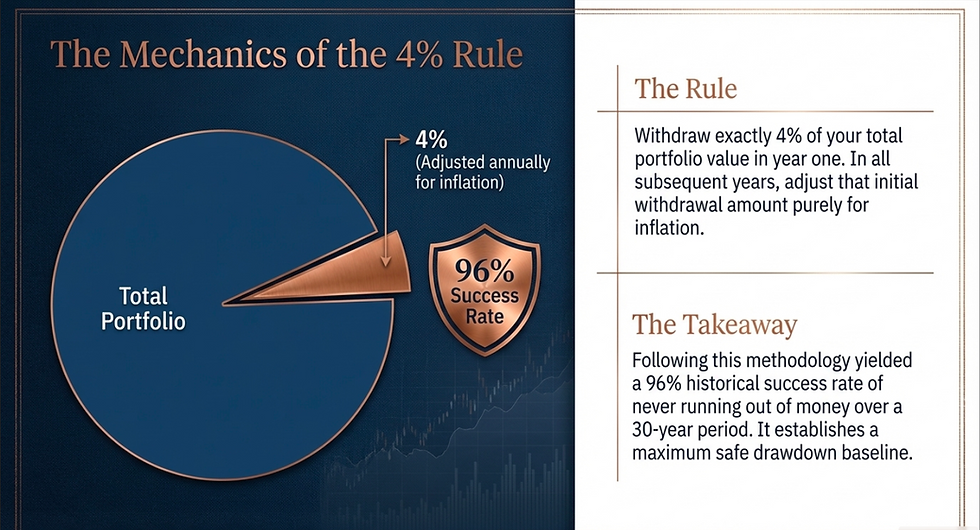

Their finding was deceptively simple. Looking at historical market data going back to 1926, they calculated that a retiree who withdrew 4% of their portfolio in year one, and then adjusted that amount annually for inflation, had a 96% success rate of never running out of money over a 30-year retirement — provided the portfolio was invested in a reasonable mix of equities and bonds.

That number — 4% — became one of the most powerful tools in personal finance. And it has a direct, concrete implication for how much you need to accumulate before you can retire.

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. He applies evidence-based frameworks like the Trinity Study to help UK SIPP investors build portfolios that can actually fund the retirement they want.

What the 4% Rule Actually Means

The 4% rule is not a prediction. It is a historically grounded rule of thumb that tells you the maximum rate at which you can draw down your portfolio each year without a high probability of running out of money over a 30-year retirement.

The inverse of 4% is 25. Multiply your desired annual retirement income by 25 and you have your target pot. This is the single most useful calculation in retirement planning:

Want £30,000/year in retirement? You need £750,000

Want £40,000/year? You need £1,000,000

Want £60,000/year? You need £1,500,000

PLSA ‘comfortable’ retirement (£37,300/year)? You need £932,500

The state pension currently pays approximately £11,500/year (2026/27 full new state pension). That reduces the income your private pension must fund — but it does not change the fundamental maths. A comfortable retirement for most professional households requires private pension income of £25,000–£50,000/year above the state pension, implying a private pot of £625,000–£1,250,000.

The Trinity Study: What the Research Actually Says

The original 1998 Trinity Study — formally titled “Retirement Savings: Choosing a Withdrawal Rate That Is Sustainable” by Cooley, Hubbard, and Walz — tested different withdrawal rates against historical market data from 1926 to 1995.

Their key findings for a 30-year retirement:

3% withdrawal rate: 100% success rate across all portfolio types

4% withdrawal rate: 96% success rate for a 75% equity / 25% bond portfolio

5% withdrawal rate: 82% success rate — meaningfully riskier

6% withdrawal rate: 68% success rate — a significant probability of running out

The 4% rule was validated in subsequent research and has been widely adopted as the planning standard. More recent analysis suggests that in today's lower-interest-rate environment, a slightly more conservative 3.5% may be appropriate for very long retirements — implying a target of 28.5x your desired annual income rather than 25x.

Why the 4% Rule Matters for UK SIPP Investors

The 4% rule was modelled on US market data and dollar-denominated portfolios. But the underlying principle — that a well-diversified equity portfolio can sustain a 4% annual withdrawal over 30 years with very high probability — applies broadly to any globally diversified portfolio.

For UK SIPP investors, the critical implication is this: the 4% rule only works if your portfolio actually grows at a rate that supports it. A managed pension fund returning 6% net — with 1.5% in annual charges consuming the rest — barely keeps pace with inflation in real terms, let alone grows your pot to the required target. A self-directed SIPP targeting 11–13% annually changes the maths entirely.

The Maths: How Growth Rate Changes Your Retirement Date

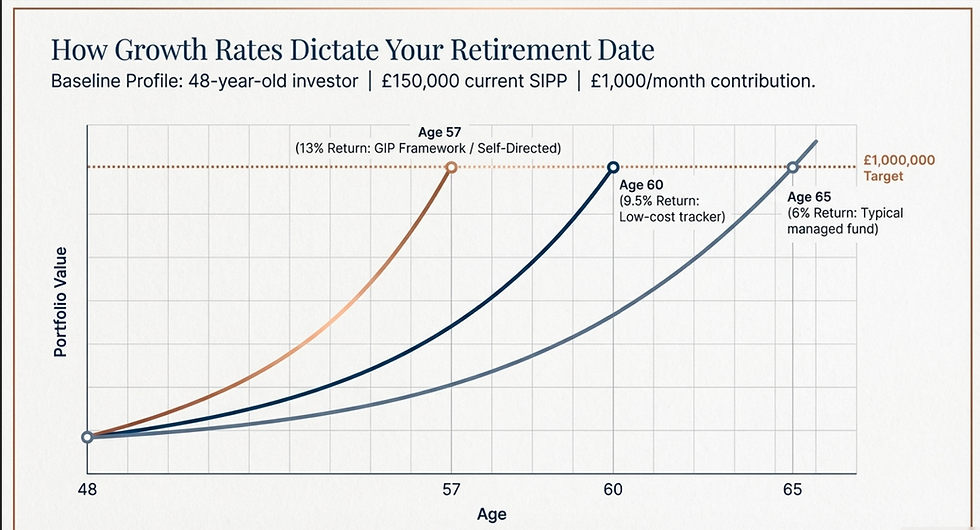

Take a 48-year-old with £150,000 in a SIPP and a target of £1,000,000 (comfortable retirement at £40,000/year using the 4% rule). Contributing £1,000/month:

At 6% (typical managed fund): reaches £1M at approximately age 65 — just on target

At 9.5% (low-cost tracker): reaches £1M at approximately age 60 — five years earlier

At 13% (GIP framework): reaches £1M at approximately age 57 — eight years earlier than managed fund

The difference between a 6% managed fund and a 13% self-directed portfolio is not just more money at the same retirement date — it is potentially retiring eight years earlier. Model your own scenario at campaignforamillion.com/tools.

Limitations of the 4% Rule — and How to Think About Them

The 4% rule has critics, and their concerns are worth understanding. The original study used US market data — arguably the strongest equity market in history. It assumed a static portfolio allocation. It did not account for tax wrappers, state pension income, or the ability to flex spending in down markets.

For UK SIPP investors, a sensible approach is to use the 4% rule as a planning floor, not a ceiling. If you build to the 25x target using a higher-growth portfolio, the 4% rule becomes very conservative indeed — because your portfolio continues compounding above the withdrawal rate. The investors who get into trouble with the 4% rule are those who arrive at retirement with just enough — accumulated via a low-growth managed fund — with no margin for error.

Frequently Asked Questions: The 4% Rule and Trinity Study

What is the Trinity Study?

The Trinity Study is a 1998 academic paper by Cooley, Hubbard, and Walz of Trinity University, Texas. It analysed historical US market data from 1926 to 1995 to determine what annual withdrawal rate a retiree could sustain over 30 years without running out of money. The paper found that a 4% withdrawal rate had a 96% success rate for a 75% equity / 25% bond portfolio — giving rise to the widely used '4% rule' of retirement planning.

Does the 4% rule apply to UK pension investors?

Broadly yes, with some adjustments. The original data was US-centric, but globally diversified portfolios show comparable long-run characteristics. UK SIPP investors should also account for state pension income (approx. £11,500/year at full new state pension rate), which reduces the income burden on the private pot. A conservative UK application might use 3.5% rather than 4% for very long retirements.

How much do I need to retire on £40,000 a year in the UK?

Using the 4% rule: £40,000 × 25 = £1,000,000 total pot required. If you receive the full state pension (£11,500/year), your private pension only needs to fund £28,500/year, implying a private pot of approximately £712,500. Run your specific scenario at campaignforamillion.com/tools to account for your actual state pension forecast and contribution schedule.

Is the 4% rule still valid in 2026?

The core finding holds. Updated analysis incorporating post-1995 data, including the dot-com crash and 2008 financial crisis, still supports a 4% withdrawal rate for portfolios with meaningful equity exposure. Some researchers recommend 3.5% as a more conservative baseline for long retirements. The key variable is portfolio growth rate — which makes the choice of investment approach critically important.

What if my pension won't reach the 4% rule target?

This is where growth rate becomes the primary lever. Switching from a 6% managed pension fund to an 11% self-directed approach has a larger impact on your final pot than any contribution increase you can realistically make in your 40s or 50s. The Great Investments Programme provides the quantitative framework and mentoring to help analytically capable professionals make that transition. Details at alpeshpatel.com/shares.

Calculate your own target retirement pot and see whether your current trajectory reaches it at campaignforamillion.com/tools. If there is a gap, book a free portfolio review and Alpesh's team will show you what closing it looks like.

Related reading: Average UK Pension Pot by Age — How to Take Control of Your SIPP — Free Pension Calculator

Disclaimer: This article is for educational purposes only and does not constitute personal financial guidance. The Trinity Study figures are historical and do not guarantee future outcomes. All investing carries risk. Past performance is not a reliable indicator of future results.

Alpesh Patel OBE

Comments