The Stoic’s Edge: Why Your Portfolio’s Volatility Isn't a Bug, It’s a Feature

- chandni54

- 2 days ago

- 4 min read

It is a curious facet of human psychology that, regardless of how many decades we spend in the arena, it remains "always both surprising and disappointing when stocks don’t always go up."

We are rational until the news cycle turns. A headline about insurance regulations, a shift in political winds, or a cooling of the AI fever, and suddenly our confidence evaporates. We look at a multi-billion-pound enterprise and convince ourselves it is "toast" simply because the ticker tape is red.

But the market is a mirror that reflects our own insecurities back at us. The Stoic investor understands that the market is entirely indifferent to our feelings, our timelines, and our ego.

To survive and thrive, one must stop treating volatility as a malfunction and recognize it as the very price of admission for long-term wealth.

The "Ownership Fallacy" and the Limits of Power

There exists a pervasive, subconscious delusion I call the "Ownership Fallacy"—the belief that our personal conviction should somehow stabilise an asset. We feel that if we have done the work and taken the position, the market should take note and reward our discernment with a smooth, upward trajectory.

In reality, the market does not grant special dispensations for reputation or status. Even the titans of industry—the Musks, the Trumps, the Buffetts—cannot command a stock to move in a single, vertical direction. I often find a certain humor in our collective hubris regarding this lack of control.

"Even Trump and Elon and Warren Buffett cannot make their names move their prices in one vertical direction. But these are lesser men so I am surprised my lack of powers at suspension :-) ... the markets taking note that if Alpesh owns it then we must be happy and ensure it only goes up."

This self-deprecating nod to our "lack of powers" is a necessary reality check. If the "gods of finance" are subject to the laws of market gravity, the private investor must accept that their ownership does not create a floor under the price.

Even Greatness Requires a 50% Drawdown

The path to legendary wealth is not a steady climb; it is a series of jagged peaks and terrifying valleys. Warren Buffett is frequently cited for his compounding success, but rarely for the stomach-churning volatility he endured to achieve it.

The 50% Milestone of Success On his journey to becoming the wealthiest man on earth, Buffett watched his entire portfolio sink by 50 percent on three separate occasions. Let that sink in.

The greatest investor of our time lost half his paper wealth three times over. The differentiator between a professional strategist and an anxious amateur is not the absence of loss, but the ability to remain "relaxed" when the move is consistent with historical norms.

Success requires the temperament to watch your best ideas get cut in half without abandoning the strategy.

The Danger of the Single-Stock "Sanity Check"

A common symptom of investor anxiety is the "Sanity Check" trap. When a private investor sees specific holdings—perhaps an insurance play like BRO or AJG—down 36-38%, they instinctively seek external validation. They want to know if "anything has changed" with the fundamentals.

This is the classic mistake of the private investor: seeking a fundamental explanation for what is often merely a "historic move." We send out data on monthly historic moves precisely to provide a benchmark for sanity.

If a stock’s decline falls within its historical range of volatility, the company isn't "toast"—it’s simply being a stock. "Sanity" isn't a feeling of comfort; it is the data-driven realization that a temporary price fluctuation is not a fundamental failure.

The 75% Trap – Why Predictions are "Lies"

The psychological torture of a drawdown is perhaps best illustrated by Meta’s recent history. The stock suffered a staggering 75 percent collapse. At the bottom, the "false prophets" of Wall Street were falling over themselves to explain why the company was finished.

What followed was a 300 percent rally that left the doomsayers in the dust.

The brutal reality is that no one has a crystal ball.

Anyone claiming they can guess whether a 75% fall is a permanent impairment of capital or a precursor to a massive rally is selling you a fantasy.

"Anyone telling otherwise is lying."

Accepting this uncertainty is the Stoic’s greatest defense. By admitting we cannot predict the exact pivot point, we insulate ourselves from making emotional decisions at the very moment when the greatest gains are often born.

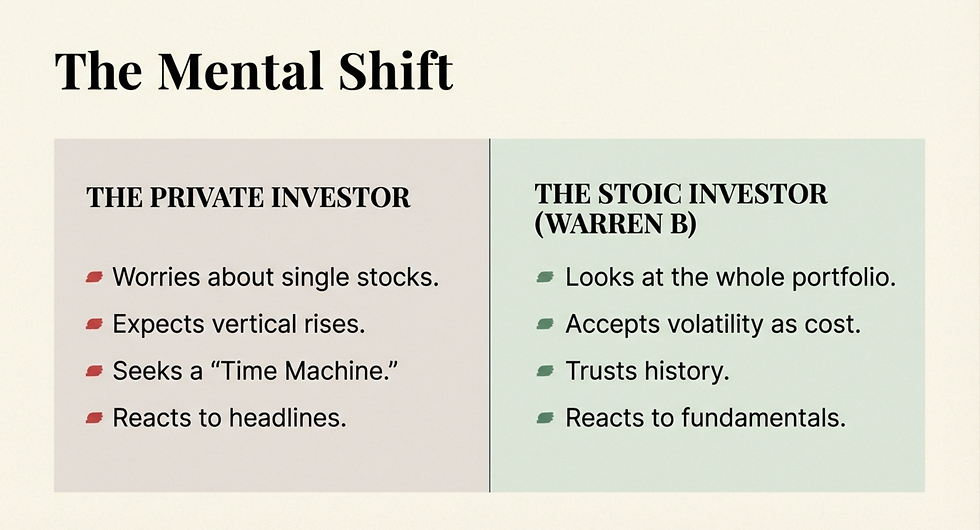

The "Warren B" Mental Shift

The ultimate solution to volatility is a fundamental shift in identity. You must stop thinking like a "private investor" and start adopting the internal temperament of "Warren B" (Buffett).

The private investor is haunted by the "Time Machine trip"—the siren song of regret that makes them wish they could go back and fix an entry price or exit a falling position. They live in the past, paralyzed by "what ifs." The "Warren B" mindset, however, lives in the present and the future.

This shift is structural as well as psychological. It is why we hold a diversified portfolio rather than a single conviction. Diversification is your defence against the urge to micromanage a single falling equity.

By holding multiple positions, you gain the breathing room to let the "historic moves" play out without feeling the need to rewrite history.

Conclusion: Moving Toward an Investment "Sanity"

True investment sanity is found in the gap between unrealistic expectations and historical reality.

To build a portfolio that lasts, you must stop viewing volatility as a bug to be fixed and start seeing it as the fuel for long-term returns. If your assets are moving within their historical norms, the only thing that needs "fixing" is your reaction to them.

Ask yourself: Do you have the Stoic temperament to watch your best ideas drop 50% on the way to long-term success, or are you still waiting for the market to take note of what you own?

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Investors should conduct their own research or seek independent advice before making investment decisions.

Alpesh Patel OBE

Comments