How Much Do You Need to Retire in the UK? The Real Number

- Alpesh Patel

- Apr 13

- 4 min read

Updated: Apr 20

Most people approaching retirement have no idea what their retirement number actually is. They have a vague sense it should be ‘quite a lot’ — but have never calculated the specific pot size needed to generate the specific income they want for the specific number of years they expect to live. This post gives you the framework to get that number right.

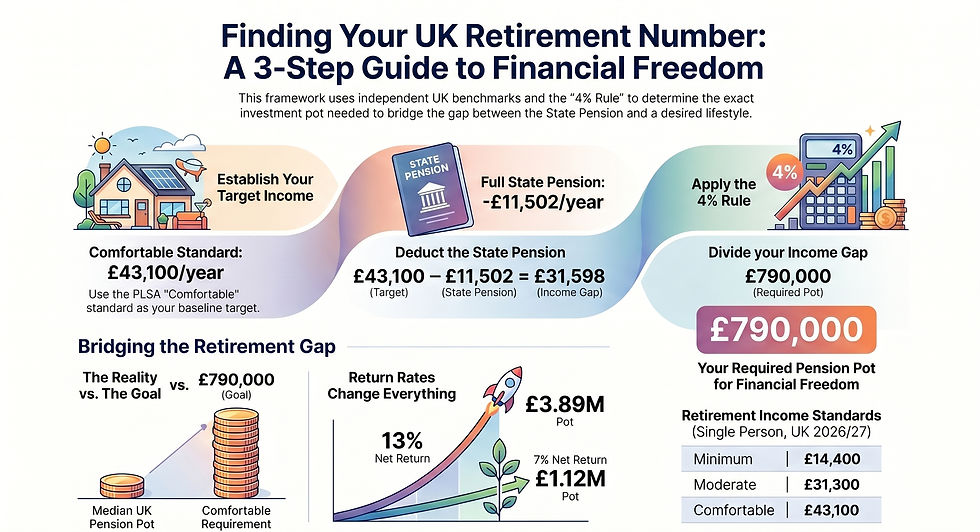

The Pensions and Lifetime Savings Association publishes annual Retirement Living Standards — the most comprehensive independent benchmark for retirement income needs in the UK. For 2026/27, the figures for a single person in the UK are: minimum standard £14,400 per year, moderate standard £31,300 per year, and comfortable standard £43,100 per year. These are real, researched figures based on what actual households spend, not estimates.

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. Calculating the retirement number is the starting point of every GIP portfolio review.

Step 1: Establish Your Target Income

Start with the PLSA standard that matches your lifestyle expectations. For most GIP members — professionals in their 40s and 50s with current income above £60,000 — the comfortable standard of £43,100 is the appropriate baseline.

Some will need more. Very few will genuinely need less if they have spent their working life at professional income levels and intend to maintain a similar standard of living in retirement.

Step 2: Subtract the State Pension

The full new State Pension for 2026/27 is £11,502.40 per year (assuming 35 qualifying years of National Insurance contributions). This is not means-tested — it is a flat entitlement. It forms the foundation of your retirement income. For most people, the State Pension is the most valuable guaranteed income source they will ever receive.

Target income (comfortable): £43,100. State Pension: £11,502. Gap that your SIPP and ISA must close: £31,598 per year. This is the number your portfolio must generate in drawdown.

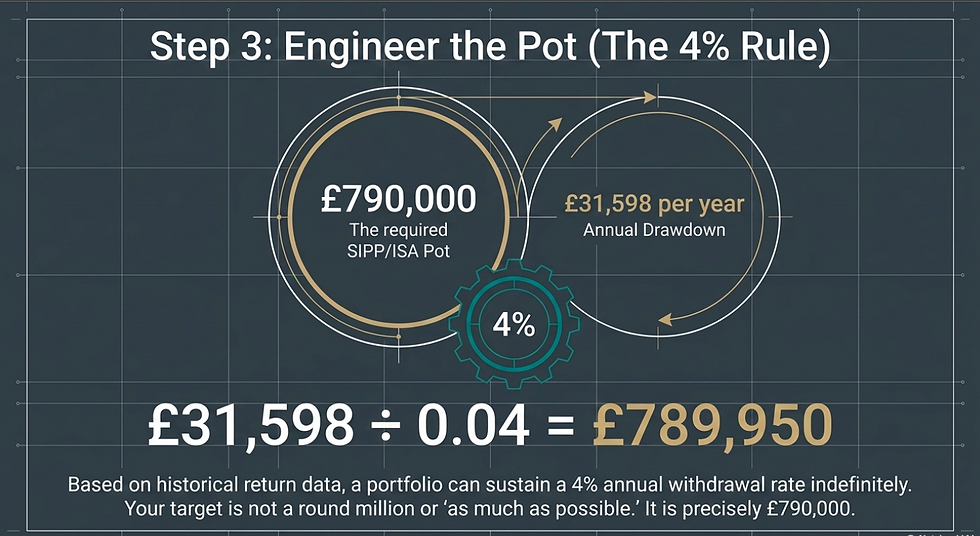

Step 3: Calculate the Required Pot Using the 4% Rule

The 4% rule states that a portfolio can sustain a 4% annual withdrawal rate indefinitely based on historical return data. Dividing the required annual income by 4% gives you the required pot size. To generate £31,598 per year: £31,598 ÷ 0.04 = £789,950. Call it £790,000.

That is your retirement number for a comfortable retirement on the PLSA standard. Not a round million. Not ‘as much as possible’. £790,000 in your SIPP and ISA combined, generating 4% per year in drawdown alongside the full State Pension.

Step 4: How to Get There — The GIP Path vs the Default Path

Starting with £150,000 in your SIPP at age 45, and contributing £1,500/month gross (£900 net as a 40% taxpayer) until 65:

Default managed fund at 7% net: Final pot approximately £1,120,000. Exceeds the retirement number. But only narrowly, and requires 20 years of contributions at this rate.

GIP framework at 13% net: Final pot approximately £3,890,000. More than five times the retirement number, giving genuine financial freedom: the ability to retire earlier, leave a significant estate, or simply withdraw more than the minimum.

The difference between meeting the retirement number and having genuine financial freedom is not the contribution rate. It is the return rate. And the return rate is determined by the investment framework.

Frequently Asked Questions

How much do I need to retire at 60 in the UK?

At 60, you cannot yet access the State Pension (currently payable at 66, rising to 67 by 2028). Your SIPP and ISA must cover 100% of your income needs from 60 to 66 — and then the State Pension kicks in. For a comfortable retirement from 60, you need a pot large enough to sustain £43,100 per year independently until 66, and then £31,598 per year (after State Pension) from 66 onward. At 4% withdrawal rate, you need approximately £1,078,000.

Is £1 million enough to retire in the UK?

£1 million at 4% generates £40,000 per year in drawdown. Combined with the full State Pension of £11,502, total income is £51,502 per year — above the PLSA comfortable standard of £43,100. For most people retiring at 65 or later, £1 million is a comfortable retirement. For those retiring earlier (before State Pension age), requiring higher income, or in a higher-cost part of the UK, more may be needed.

What is the average UK pension pot at retirement?

According to DWP and ONS data, the median private pension wealth for those aged 55–64 in the UK is approximately £107,000. The mean (average, pulled higher by large pots) is approximately £185,000. Both figures are significantly below the £790,000 needed for a comfortable retirement. This is the retirement savings gap that the GIP framework is designed to close.

To calculate your own retirement number and model how the GIP framework gets you there, book a free portfolio review here

Sources & Further Reading

PLSA — Retirement Living Standards 2026/27: minimum, moderate, and comfortable income benchmarks. plsa.co.uk

DWP — Pension Wealth in Great Britain: Wealth and Assets Survey. Private pension wealth distribution by age and gender. gov.uk/government/collections/wealth-in-great-britain-survey

Bengen, W.P. (1994) — 'Determining Withdrawal Rates Using Historical Data'. Journal of Financial Planning. The 4% rule research underpinning sustainable drawdown rates.

HMRC — State Pension rates 2026/27. gov.uk/new-state-pension/what-youll-get

Disclaimer: This article is for educational purposes only. Retirement income projections are illustrative. All investing carries risk. The 4% rule is a guideline based on historical data and is not a guarantee. This does not constitute personal financial guidance.

Alpesh Patel OBE

Comments