Does Diversification Still Work in a World of Correlated Assets?

- Alpesh Patel

- Oct 26, 2025

- 6 min read

Introduction

Diversification is the oldest proverb in finance: “Don’t put all your eggs in one basket.” Yet in a world where global markets move together - where U.S. tech selloffs drag down Asian indices, and bond prices fall alongside equities - the wisdom of that proverb seems increasingly hollow.

This essay argues that diversification still works, but differently. Traditional cross-asset diversification has weakened in a highly globalised, liquidity-driven world, yet diversification across risk factors, time horizons, and strategies remains both viable and essential. The failure lies not in the principle, but in investors’ outdated interpretation of it.

1. The Classical Case for Diversification

Modern Portfolio Theory (Nobel Prize Winner – Harry Markowitz, 1952) formalised diversification as the optimisation of expected return for a given level of risk.

The logic rests on imperfect correlation: when assets do not move in lockstep, portfolio volatility falls faster than returns decline, improving risk-adjusted performance.

Put in simple terms, imagine two companies giving average returns of 15% in a year, but they when one is rising the other is falling and vice versa.

You get 15% return (because that’s their average annual return) but they cancelled each other’s volatility out. So combined you had less risk ie volatility than with each one separately.

Or, two risky assets combined, make a less risky portfolio - so diversify. Nobel Prize!

In the 1980s and 1990s, this model appeared unassailable.

Bonds zigged when equities zagged; commodities hedged inflation; emerging markets offered growth uncorrelated with the developed world. The global efficient frontier seemed broad and attainable.

But the financial system of 2025 is not that of 1985. Correlations have converged.

2. The Great Correlation Convergence

Globalisation, monetary policy coordination, and algorithmic trading have tightened linkages across asset classes. During stress periods, correlations tend toward one.

Empirical evidence is sobering:

During the 2008 crisis, equity–bond correlations flipped positive for the first time in decades as both asset classes fell simultaneously.

In March 2020, at the onset of the COVID-19 panic, the MSCI World Index and U.S. Treasuries both declined as investors liquidated everything for cash.

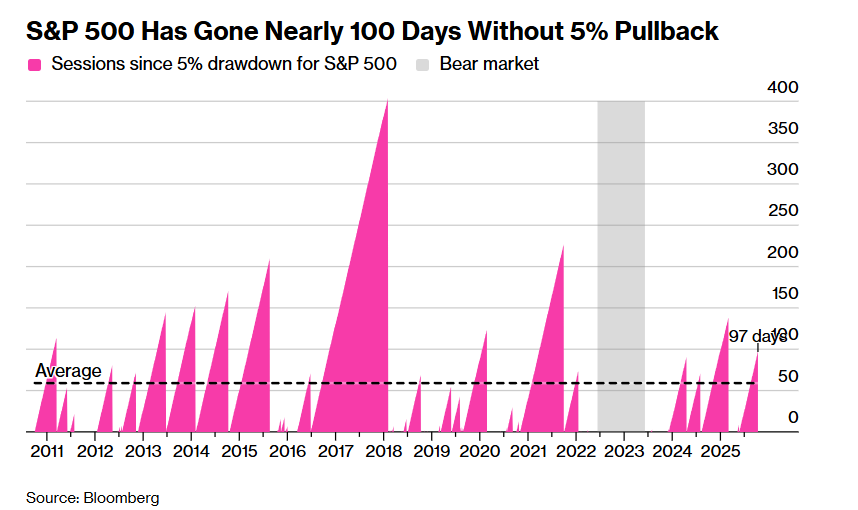

Even in 2022, inflation shocks drove simultaneous sell-offs in equities and bonds -the worst combined performance for a 60/40 (equities/bonds) portfolio since 1937 (Morningstar, 2023).

The old “risk-off” asset classes no longer offer reliable refuge. In a world governed by central bank liquidity, risk assets now dance to the same monetary tune.

Worse still, those who went to University in the 1980s never kept up with their education. They remembered old outdated text books.

3. Why Correlation Is Not Constancy

Yet the declaration that “diversification is dead” is premature. Correlation is contextual, not constant. It spikes in crises but mean-reverts in stability.

As Asness et al. (AQR, 2015) noted, “Correlations are highest when diversification is most valuable - but also when investors are least able to use it.”

It’s something I have written about in the my Financial Times column – when you need diversification the most, you’re least likely to get it. Ie markets correlate to the downside.

Moreover, correlation measures directional movement, not magnitude of risk. Two assets can fall together but by different amounts; a 3% equity drawdown cushioned by a 0.5% bond decline still softens the blow.

Diversification is therefore not about eliminating loss but reducing variability of loss. In that sense, it continues to function, albeit less dramatically than textbooks promise.

4. Factor Diversification: Beyond Asset Classes

The failure of traditional diversification arises from thinking in asset labels (stocks, bonds, property) rather than in underlying risk factors.

Academic research since Nobel Prize Winner Fama and French (1993) shows that returns derive from common factors - value, momentum, size, quality, and low volatility.

Two “different” assets may share identical factor exposure. Owning U.S. tech and Chinese tech, for instance, is not diversification - it is duplication.

Modern portfolios therefore seek factor diversification, not just asset diversification. By balancing exposures to growth, inflation, credit, and liquidity risks, investors achieve more robust resilience across regimes.

The GIP model portfolio, for instance, uses Sortino-weighted Quality-Growth-Income filters to ensure that no single macro driver dominates long-term performance.

The goal is to diversify why returns occur, not just where.

5. Temporal Diversification: The Role of Time

A second dimension is temporal diversification - spreading exposure across time horizons.

Thus, temporal diversification - staying invested across cycles - remains the most under appreciated form of protection. Volatility compresses in the long run, but investor patience rarely lasts that long.

6. Structural Diversification: Geography and Policy Regimes

The modern economy is globally integrated but politically fragmented. Structural diversification, therefore, means allocating across policy regimes, not just countries.

Investors exposed solely to Western monetary policy face synchronous risk: when the Fed tightens, the Bank of England and ECB follow.

But emerging markets with independent cycles - such as India or Indonesia - offer genuine diversification.

Similarly, real assets like infrastructure or renewable energy are influenced by regulation, not just markets.

Their cashflows depend on policy stability rather than interest rates, offering structural resilience when financial assets correlate.

7. The Behavioural Edge: Diversification as Psychological Armour

Diversification is as much behavioural as mathematical. During crises, diversified portfolios cushion psychological stress, helping investors stay invested.

The FCA (2023) found that UK investors who maintained globally diversified portfolios during 2022’s drawdowns had 35% lower redemption rates than those concentrated in single markets.

In behavioural finance terms, diversification lowers loss salience - the emotional sting of drawdowns - thus preserving long-term compounding. Even if correlations rise, smoother performance keeps investors disciplined.

The greatest diversification benefit, therefore, may be behavioural survival, not statistical reduction of variance.

8. The New Diversification Frontier: Strategies, Not Securities

Finally, diversification in 2025 extends to strategy diversification: systematic trend-following, volatility harvesting, and market-neutral approaches that profit from dispersion, not direction.

The Yale Endowment model - between 2000 and 2020, Yale achieved a Sharpe ratio nearly double that of the S&P 500 with lower drawdowns, primarily through uncorrelated strategies rather than uncorrelated assets.

Artificial intelligence and data-driven models now allow dynamic correlation monitoring, enabling portfolios that adapt to changing regimes rather than assuming static relationships.

Diversification, in short, has become an active verb. In GIP our twice weekly market updates and constant monitoring ensure we do not lose track of this.

Conclusion

Diversification has not died - it has matured. In a world of correlated assets, investors must diversify across factors, timeframes, regimes, and strategies rather than merely securities.

The illusion of independence has vanished; the necessity of balance has not.

The danger lies not in correlation itself but in complacency: treating diversification as a one-off structure rather than a living process.

As global shocks synchronise markets, only adaptive, multi-dimensional diversification can keep portfolios resilient.

So yes, diversification still works - just not the way your grandfather’s portfolio did. In the modern era, it works precisely because investors keep redefining what it means.

Sources:

Markowitz, H. (1952). Portfolio Selection. Journal of Finance.

Fama, E. & French, K. (1993). Common Risk Factors in the Returns on Stocks and Bonds. Journal of Financial Economics.

Asness, C., Frazzini, A., & Pedersen, L. (2015). A Century of Evidence on Trend-Following Investing. AQR.

Dimson, E., Marsh, P., & Staunton, M. (2024). Credit Suisse Global Investment Returns Yearbook.

Morningstar (2023). The 60/40 Portfolio: Post-Mortem or Rebirth?

FCA (2023). Retail Investment Behaviour Report.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Past performance and historical drawdowns do not guarantee future results. Investors should assess their individual circumstances or seek regulated advice before making investment decisions.

Alpesh Patel OBE

Comments