Long Term Investing: Why $100 Became $43,000 And How You Can Start Your Journey

- Alpesh Patel

- Feb 25

- 4 min read

Most investors underestimate just how powerful long term investing can be especially when it comes to building a comfortable retirement.

If you had invested $100 in 1965 and done nothing else but stay invested, your wealth in 2025 would have looked very different depending on the asset you chose:

$43,000 in stocks

$12,000 in gold

$9,200 in corporate bonds

$2,800 in government bonds

$2,100 in real estate

$1,500 in cash

That’s the dramatic result of compounding returns over time and it provides the strongest argument for building long-term pension wealth through disciplined investing.

Most investors overestimate what they can achieve in one year and massively underestimate what long term investing can do over decades.

The image above tells a simple but uncomfortable truth. If you invested just $100 in 1965 and did nothing clever, nothing complex, nothing exciting, just stayed invested the outcome by 2025 would have depended entirely on what you owned.

The difference between stocks and cash wasn’t skill. It wasn’t timing. It wasn’t intelligence.

It was compounding over time the single most important force behind successful pensions and lifetime wealth.

This is where the Great Investments Programme and the suite of tools at CampaignForAMillion.com become indispensable.

Long Term Investing Returns: One Decision, Six Very Different Outcomes

Let’s start with what the data actually shows.

Over 60 years:

Stocks turned $100 into $43,000

Gold became $12,000

Corporate bonds grew to $9,200

Government bonds reached $2,800

Real estate ended around $2,100

Cash barely made it to $1,500

This means stocks delivered:

29x the return of cash

Over 3.5x the return of gold

Nearly 5x the return of government bonds

That gap is not explained by luck.It’s explained by long term investing plus compounding.

Why Long Term Investing Works: Compounding Is Your Secret Weapon

Compounding isn’t linear, it accelerates over time. That’s why investments held over decades far outperform short-term gambles or frequent trading.

In long term investing:

The first 10–20 years builds the foundation

The next 20 sets the growth phase

The final 20 delivers the real wealth

This is exactly how pensions grow; through consistency, patience, and repetition.

Instead of guessing market direction, you let time do the heavy lifting. Miss the last phase by selling early, panicking, or staying in cash and you miss most of the upside.

This is also why short-term thinking destroys pensions.

Long Term Investing and Pensions: The Silent Wealth Gap

Pensions are not supposed to be exciting.They are supposed to be effective.

Yet millions of savers sit in:

Over-conservative default funds

Cash-heavy allocations

Low-growth strategies designed to “feel safe”

The irony? Cash is the riskiest asset for long-term savers.

It quietly guarantees:

Loss of purchasing power

Underfunded retirements

Dependence instead of independence

Long term investing is not about avoiding volatility, it’s about embracing growth where time absorbs risk.

The Campaign For A Million Tools: Your Long Term Investing Engine

Understanding the power of compounding is one thing, acting on it is another.

That’s why the tools at CampaignForAMillion.com were created: to help you build, manage and monitor long-term growth in line with your retirement goals.

Here’s how they help:

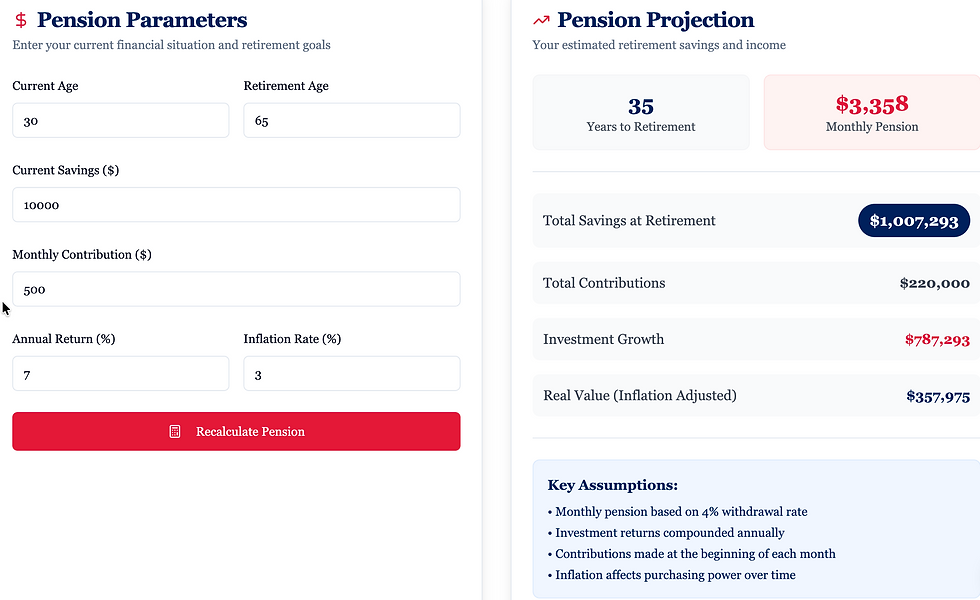

Example: Using the Growth Simulator to Plan a Pension

Let’s say you’re 30 years old and want to see where your retirement savings might end up by age 65.

If you enter the following into the Growth Simulator:

Current savings: £10,000

Monthly contribution: £500

Expected annual return: 7%

Time horizon: 35 years

The tool will show you how your money could compound, giving you a clearer picture of what long-term investing can achieve - and how close you might be to your million-pound goal.

Use the Growth Simulator, Risk Profile Analyser, and Diversification Planner to build a strategy that reflects your goals and risk tolerance: https://www.campaignforamillion.com/tools

Long Term Investing Is a Behavioural Game, Not an IQ Test

The biggest enemy of long term investing isn’t volatility.

It’s:

Panic selling

News-driven decisions

Over-trading

Switching strategies mid-cycle

The investors who turned $100 into $43,000 didn’t “do more”.

They did less and stayed invested.

That lesson applies directly to:

Pensions

ISAs

Long-term portfolios

Retirement planning

Long Term Investing and Your Pension: Don’t Let Time Go to Waste

Many pension savers fall into one of two traps:

Being too conservative, which means losing value to inflation

Being too reactive, which means selling at the worst times

Both destroy the magic of compounding.

By using the Campaign For A Million tools and leaning into the principles of long term investing, you:

Define a clear trajectory

Avoid emotional decision-making

Unlock more wealth over time

That’s the difference between a pension that keeps up with inflation and one that builds real financial freedom.

Your Roadmap to a Million - Start With a Plan

Here’s a simple step-by-step way to use the tools:

Assess Your Risk Profile: Know how much risk you can tolerate

Simulate Growth: Project where your savings could be in 10, 20, 30+ years

Diversify Smartly: Understand how asset allocation affects your outcomes

Set Regular Contributions: Use automation to stay disciplined

Review Progress Annually: Let compounding grow your future automatically

All of this is available at CampaignForAMillion.com with tools designed to empower every investor, whether you’re just starting or deeply focused on retirement planning.

Long Term Investing Is Boring and That’s the Point

If your pension feels dull, it’s probably working.

If your strategy relies on constant action, it’s probably broken.

The data is clear:

Time matters more than timing

Ownership beats speculation

Compounding rewards patience

Long term investing isn’t about predicting the future.

It’s about not getting in the way of it.

Your Pension Deserves Long Term Investing

The data doesn’t lie:

The longer you stay invested, the more compounding rewards you

Stocks have historically delivered the highest returns over time

Cash and low-yield assets simply don’t keep up with inflation

If you want your pension to work as hard as possible, you need a plan, not hope.

The Campaign For A Million tools give you clarity, direction, and control over your long-term investing journey.

Start here: https://www.campaignforamillion.com/tools

Risk Warning: Capital at risk. Past performance is not a reliable indicator of future results. This article is for educational purposes only and does not constitute financial advice. Alpesh Patel OBE www.campaignforamillion.com

Comments