Investing in Your 50s UK 2026: The Last Decade to Change Your Retirement Outcome

- Alpesh Patel

- Apr 19

- 7 min read

Updated: Apr 30

Investing in your 50s UK is different from investing in your 40s in one critical respect: the decisions you make now are the last ones that will materially change your retirement outcome. A 52-year-old with £200,000 in a SIPP has 13 years of compounding runway to age 65. At 13% CAGR that £200,000 becomes £962,000. At the 7% default managed fund average it becomes £491,000. The gap between those two outcomes is £471,000, and it is determined entirely by what happens in the next decade.

Why Investing in Your 50s in the UK Is the Decisive Decade

The 50s are the decade where the most powerful variables in retirement wealth are still changeable. Earnings are typically at or near their peak. Children have often moved through full-time education.

Mortgage debt is reduced or cleared. These factors combine to produce the highest disposable income available for pension contributions at precisely the moment when compounding has 10 to 15 years to work before retirement.

DWP Wealth and Assets Survey 2022 data showed that the median private pension wealth for UK adults aged 55 to 64 is approximately £107,000, the mean approximately £185,000. Both figures are sharply below what a comfortable retirement requires at PLSA standards.

Sequence of returns risk, documented by Blanchett and Kaplan in their 2012 Morningstar research, is the primary risk that distinguishes investing in the 50s from investing in the 40s. A severe bear market in the five years before or after retirement can permanently impair a portfolio because large withdrawals taken during a drawdown lock in losses that the portfolio cannot recover from.

This is not a reason to reduce equity exposure uniformly in the 50s, which the FCA Retirement Outcomes Review 2018 identified as a major cost of default lifestyle funds. It is a reason to own businesses with high CROCI scores and low Calmar drawdown ratios, which retain more value during market falls.

What Investing in Your 50s UK Actually Looks Like: The Six Actions That Matter

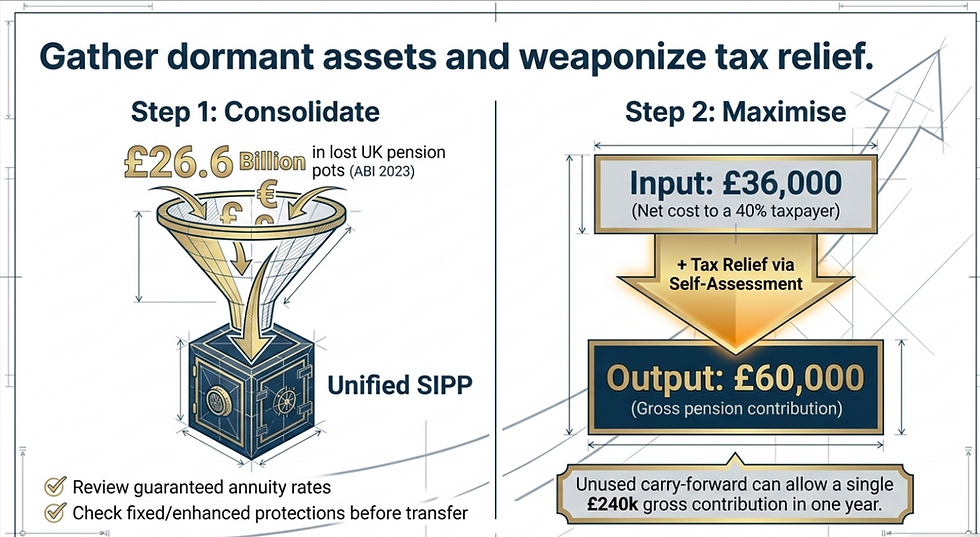

First, consolidate every defined contribution pension pot you hold. The Association of British Insurers estimated in 2023 that £26.6 billion sits in lost or dormant UK pension pots. Tracing and consolidating them into a single self-directed SIPP gives you visibility, removes duplicate platform fees, and allows a single systematic framework to run across the whole.

Use the government's Pension Tracing Service at gov.uk/find-pension-contact-details. Before transferring, check for guaranteed annuity rates, fixed protection, and enhanced protection arrangements that may be lost on transfer.

Second, maximise the pension annual allowance. The 2026/27 annual allowance is £60,000 gross, including employer contributions. Most people in their 50s with a decade of solid earnings and reduced outgoings have both the income and the carry-forward allowance to contribute significantly.

Unused annual allowance from the previous three tax years can be carried forward, potentially enabling a single contribution of up to £240,000 gross in one tax year. For a 40% taxpayer, the effective cost of £60,000 gross pension contribution is £36,000 net after higher-rate tax relief claimed through self-assessment.

Third, switch from a default managed fund to a systematic investment framework. The FCA Retirement Outcomes Review 2018 found that 94% of DC pension savers remained in their default fund and had never made an active investment choice.

SPIVA 2024 UK Scorecard data shows that 87% of active UK fund managers underperformed their benchmark over 10 years. A GIP investor replacing a 7% net default fund with a 13% CAGR systematic framework over 13 years sees the compounding difference illustrated above: £962,000 versus £491,000 on a £200,000 starting pot.

Fourth, fill the ISA allowance alongside the SIPP. The £20,000 ISA allowance provides tax-free, flexibly accessible capital that can bridge the gap between any early retirement date and age 57 when the SIPP becomes accessible.

From April 2028, the minimum SIPP access age rises to 57. An investor retiring at 55 needs two years of living expenses in an accessible wrapper. An investor retiring at 52 needs five years. The ISA is the correct vehicle for this bridge capital.

Fifth, check your National Insurance record. Full new State Pension requires 35 qualifying NI years. Class 3 voluntary NI contributions cost approximately £824 per year of gaps and add approximately £329 per year to the State Pension for life. The payback period is roughly 2.5 years. For most people with gaps in their record, filling them is one of the highest-return financial actions available in their 50s. Check at gov.uk/check-state-pension.

Sixth, review platform charges in detail. The FCA SIPP market study 2023 confirmed that platform cost is the largest controllable variable in long-run SIPP outcomes after investment return. On a £300,000 SIPP over 13 years at 13% CAGR, a 0.1% annual cost difference compounds to approximately £47,000 in foregone terminal value.

For SIPP portfolios above £100,000, flat-fee platforms including Interactive Investor and, for pure equity portfolios, Trading 212, produce materially lower total costs than percentage-based platforms.

Should You De-Risk Your SIPP When Investing in Your 50s in the UK?

De-risking by shifting from equities to bonds in the 50s is the default action of lifestyle pension funds. The FCA Retirement Outcomes Review 2018 identified this as a significant source of value destruction for investors taking drawdown rather than buying an annuity.

Bonds provide a genuine hedge for annuity purchase because the annuity rate is tied to gilt yields. For drawdown investors, bonds in the 50s simply reduce long-run return without providing the growth needed to sustain 20 to 30 years of retirement income.

The GIP framework's answer to sequence of returns risk is not de-risking through asset class rotation into bonds. It is owning businesses with high Sortino and Calmar ratios that have demonstrated resilience through prior market falls.

A high-Calmar business losing 15% in a severe bear market while the broader market falls 40% produces a far better outcome in drawdown than a bond allocation that generates 2% returns in the accumulation years. The CROCI screen, applied as the first filter, specifically identifies businesses with genuine economic moats that maintain earnings and cash generation through downturns.

Frequently Asked Questions: Investing in Your 50s in the UK

Is it too late to start investing at 55 in the UK?

No. At 55 with a retirement target of 65, there are 10 years of compounding available. At 13% CAGR, £50,000 invested at 55 becomes £169,000 by 65. £100,000 becomes £339,000. The tax relief available on SIPP contributions significantly reduces the net cost. A 40% taxpayer contributing £60,000 gross per year pays £36,000 net. Over five years of maximum contributions that produces £180,000 net cost and approximately £300,000 gross pension contributions before investment growth.

How much should I have in my pension by 50 in the UK?

The PLSA Retirement Living Standards 2024 set a comfortable retirement at £43,100 per year. Subtracting the full State Pension of £11,502 leaves a £31,598 gap from private pension. At a 4% withdrawal rate, closing that gap requires approximately £790,000 in the SIPP at retirement. To reach £790,000 from age 50 with 15 years to retirement at 65 at 13% CAGR requires a starting pot of approximately £128,000 with no further contributions. The DWP 2022 data shows the median pension pot at age 55 to 64 is £107,000, significantly below this target.

Should I pay off my mortgage or invest in my pension in my 50s UK?

The comparison is between the mortgage interest rate and the net-of-tax return on pension investment. If the mortgage rate is 4.5% and the expected pension investment return is 13% before tax relief, the pension wins significantly. The additional consideration is tax relief: a 40% taxpayer contributing £10,000 to the SIPP pays £6,000 net, making the effective pension return even more attractive. If the mortgage rate exceeds 7% to 8%, the comparison becomes closer. Most GIP investors in their 50s with pension compounding to run should prioritise the pension over overpaying a sub-5% mortgage.

How do I access my SIPP at 57 in the UK?

From April 2028, the minimum pension access age rises from 55 to 57. To access the SIPP at 57, contact the platform directly to initiate flexi-access drawdown. You can take up to 25% of the pot as a tax-free lump sum, capped at £268,275 from April 2024. The remaining 75% stays invested and is withdrawn as taxable income at your marginal rate. Triggering drawdown also activates the Money Purchase Annual Allowance of £10,000, reducing future contribution capacity significantly. This is a critical reason to avoid taking pension benefits before you genuinely need to.

What is the best investment strategy for someone investing in their 50s in the UK?

The GIP framework: a portfolio of 20 to 25 global equities screened across CROCI above 10%, PEG below 1.0, Sortino above 1.0, positive Sharpe, and Calmar resilience. These screens identify businesses generating genuine economic value at reasonable prices with demonstrated resilience through market falls. The key discipline in the 50s is equal weighting positions to prevent any single stock creating catastrophic drawdown risk, and applying the Calmar screen rigorously to exclude stocks with histories of large peak-to-trough losses.

Should I de-risk my pension in my 50s by moving into bonds?

Only if you plan to buy an annuity at retirement. Annuity rates move with gilt yields, so bond holdings provide a genuine hedge for investors taking this route. For the majority of self-directed SIPP investors taking drawdown in retirement, moving into bonds in the 50s reduces return without providing a matching reduction in the risks that actually matter in drawdown. The FCA Retirement Outcomes Review 2018 documented this as the primary cost of lifestyle funds for drawdown investors. The better route is owning high-Calmar, high-CROCI equities that resist large drawdowns while continuing to compound at meaningful rates.

Sources and Further Reading

DWP Wealth and Assets Survey 2022, gov.uk/government/collections/wealth-and-assets-survey. PLSA Retirement Living Standards 2024, plsa.co.uk/retirement-living-standards. FCA Retirement Outcomes Review 2018, fca.org.uk/publications/market-studies/retirement-outcomes-review. Blanchett, D. and Kaplan, P. (2012), Alpha, Beta, and Now Gamma, Morningstar. SPIVA UK Scorecard 2024, S&P Dow Jones Indices. ABI Pension Statistics 2023, abi.org.uk. ONS Pension Wealth in the UK 2022, ons.gov.uk.

About the Author

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. He is the founder of the Great Investments Programme at campaignforamillion.com.

Disclaimer: This article is for information and educational purposes only. It does not constitute financial guidance specific to your personal circumstances. Past investment performance is not a reliable indicator of future results. Consult a qualified professional before making financial decisions.

Comments