ISA vs SIPP UK 2026: Which Should You Fill First and Why the Order Matters

- Alpesh Patel

- Apr 20

- 7 min read

Updated: May 5

For most UK higher-rate taxpayers in their 40s with no immediate need for flexible access to the money, the SIPP should be filled before the ISA. A higher-rate taxpayer contributing £10,000 net to a SIPP receives £6,667 in tax relief, making the gross contribution £16,667 and the effective net cost £6,000 after claiming higher-rate relief through self-assessment.

The ISA offers no upfront tax relief. From April 2027, however, unused pension funds will sit within the IHT estate. That changes the ISA vs SIPP UK calculation for investors with larger estates who plan to pass pension wealth to beneficiaries.

ISA vs SIPP UK: The Fundamental Difference in 2026

The SIPP and ISA are both tax-efficient wrappers but they work differently. The SIPP gives upfront tax relief at your marginal income tax rate and taxes withdrawals in retirement as income. The ISA gives no upfront relief but all growth, income, and withdrawals are tax-free.

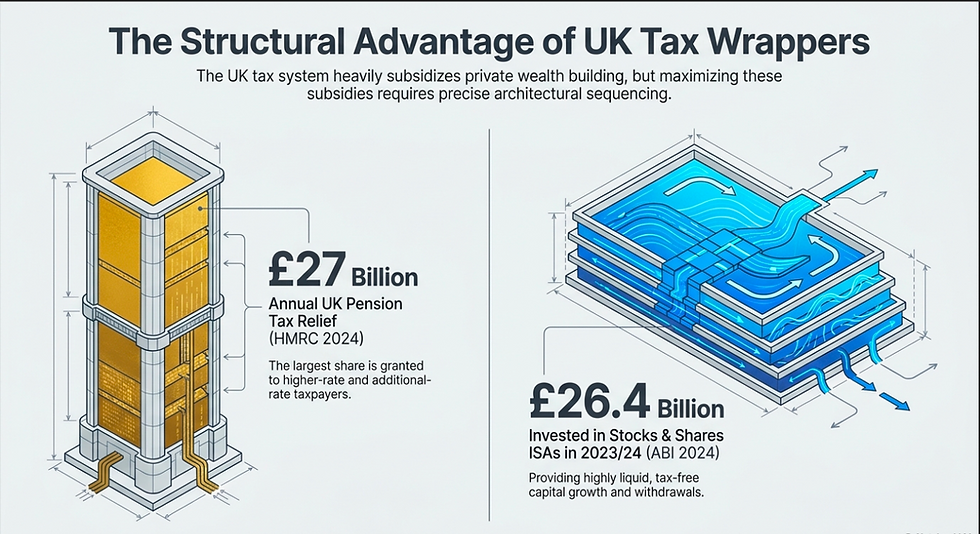

The HMRC pension tax relief statistics for 2024 estimate that approximately £27 billion in pension tax relief is granted per year in the UK, of which the largest share goes to higher-rate and additional-rate taxpayers. The ABI ISA statistics for 2024 confirm that ISA subscriptions continue growing, with £26.4 billion invested in Stocks and Shares ISAs in 2023/24.

The SIPP has three structural advantages over the ISA. First, the tax relief multiplier: a 40% taxpayer contributes £6,000 net and receives £10,000 gross in the pension, an immediate 67% uplift on the net investment. A 45% taxpayer sees the net cost fall to £5,500 for a £10,000 gross contribution.

Second, employer contributions: employed investors in workplace SIPPs receive employer matching that is unavailable for ISA contributions. Third, annual allowance: the £60,000 SIPP allowance dwarfs the £20,000 ISA allowance, enabling significantly larger tax-sheltered investment for higher earners.

The ISA has three structural advantages over the SIPP. First, flexibility: ISA funds can be accessed at any age with no tax on withdrawal, making it the correct vehicle for capital needed before age 57. Second, withdrawal tax: there is no income tax on ISA withdrawals in retirement, whereas all SIPP withdrawals above the 25% tax-free amount are taxed as income at the marginal rate.

Third, from April 2027, the inheritance tax treatment: from that date the pension joins the ISA inside the estate, removing one of the SIPP's previous structural advantages over the ISA for estate planning.

ISA vs SIPP UK 2026: Who Should Fill the SIPP First

Higher-rate taxpayers with income above £50,270 should fill the SIPP first. The 40% tax relief makes the effective SIPP contribution cost 60p for every £1 gross. If the same money were invested in an ISA instead, the full £1 must come from post-tax income with no uplift. The Vanguard research by Bennyhoff and Kahlenberg (2012) on the value of tax-efficient account selection confirmed that upfront tax relief compounding over a 20-year investment horizon produces outcomes that cannot be replicated by any other approach. The break-even requires the ISA investment to outperform the SIPP by 40 percentage points cumulatively to justify forgoing 40% tax relief on each contribution.

Basic-rate taxpayers with income below £50,270 still benefit from 20% SIPP tax relief, making the effective cost 80p per £1 gross. But the gap between SIPP and ISA tax efficiency is smaller for basic-rate taxpayers, and the ISA's flexibility advantage is more relevant for those who may need the capital before 57. The IFS analysis of pension tax relief distributional effects (2023) concluded that the SIPP subsidy is substantially more valuable for higher earners than lower earners, which is the primary political justification for ongoing review of higher-rate pension relief.

ISA vs SIPP UK: The ISA Case for Early Retirement Before Age 57

From April 2028, the minimum SIPP access age rises to 57. An investor targeting retirement at 52 cannot touch the SIPP for five years. An investor targeting retirement at 55 cannot touch it for two years. The ISA is the bridge: tax-free, flexibly accessible, no minimum age requirement. For FIRE investors, the correct vehicle stack is SIPP for the bulk of long-term accumulation where tax relief applies, ISA for the bridging capital needed from the early retirement date to age 57, and General Investment Account for any overflow above the £20,000 ISA allowance.

The FCA Retirement Outcomes Review 2018 found that the majority of drawdown investors are drawing income from pension funds that continue to compound within the wrapper simultaneously. For early retirees, the same principle applies across wrappers: the SIPP continues to compound untouched from early retirement to age 57, while the ISA provides income. From 57 onwards the SIPP drawdown begins, and the tax-free lump sum of up to £268,275 provides a meaningful one-time tax-free cash injection.

How the April 2027 IHT Change Affects the ISA vs SIPP UK Decision

Before April 2027, the SIPP had a clear IHT advantage: pension pots passed to beneficiaries outside the estate. From April 2027, unused pension funds count toward the estate. For investors with total estates above the nil-rate band of £325,000, this change reduces the SIPP's relative advantage over the ISA for estate planning. Both are now within the estate. The SIPP still wins on upfront tax relief for contributions. But for investors who accumulate more pension wealth than they can spend in retirement, the ISA becomes relatively more attractive: it offers the same IHT treatment as the post-2027 pension, with the additional advantage of tax-free income and no minimum access age.

The practical response for most investors is not to stop contributing to the SIPP. The 40% tax relief advantage on contributions is too large to abandon. Instead, investors with large estates should focus on drawing pension income up to the basic-rate threshold each year, moving funds into the ISA, and making regular gifts from surplus income. This strategy converts SIPP funds into ISA funds and cash gifts, reducing the estate exposure systematically while retaining the compounding advantage of the SIPP during accumulation.

Frequently Asked Questions: ISA vs SIPP UK 2026

Should I put money in an ISA or SIPP first in the UK?

If you are a higher-rate or additional-rate taxpayer with no need for the money before age 57, fill the SIPP first. The 40% or 45% tax relief makes each pound of net contribution worth significantly more inside the SIPP than in an ISA. If you are a basic-rate taxpayer or need flexible access to the capital before 57, the ISA's advantages are more meaningful. In most cases the correct answer for working adults with income above £50,270 is to maximise the SIPP first, then direct remaining savings into the ISA.

Can I contribute to both an ISA and SIPP in the same year in the UK?

Yes. The £60,000 SIPP annual allowance and the £20,000 ISA allowance are completely independent. You can contribute the maximum to both in the same tax year. A higher-rate taxpayer contributing £60,000 gross to their SIPP at a net cost of £36,000, and £20,000 to their ISA, would invest £80,000 into tax-efficient wrappers in a single year at a net cost of £56,000. Few investors reach both limits, but using both wrappers simultaneously is the optimal strategy for those who can.

Is a SIPP better than an ISA for retirement in the UK 2026?

For accumulation, yes: the SIPP's upfront tax relief produces larger compounding pots than an ISA funded with the same net of tax income. For retirement income, it depends on your tax position in retirement. ISA withdrawals are always tax-free. SIPP withdrawals above the 25% tax-free amount are taxed as income. If retirement income from SIPP drawdown plus State Pension pushes you into the higher-rate band, some of the accumulation-phase advantage is clawed back at withdrawal. For investors whose retirement income will stay within the basic-rate band, the SIPP accumulation advantage almost always outweighs the withdrawal tax cost.

What are the main differences between an ISA and a SIPP in the UK?

SIPP: upfront tax relief at marginal rate, employer contributions possible, annual allowance £60,000, minimum access age 57 from April 2028, withdrawals above tax-free amount taxed as income, within IHT estate from April 2027. ISA: no upfront tax relief, no employer contributions, annual allowance £20,000, accessible at any age with no tax on withdrawal, within IHT estate always. The SIPP is structurally superior for accumulation. The ISA is structurally superior for flexibility and retirement income planning where withdrawals would otherwise be heavily taxed.

Should I use my ISA or SIPP for early retirement before age 57 in the UK?

The ISA is the correct vehicle for income needed before age 57. The SIPP cannot be accessed before 57 from April 2028 without incurring an unauthorised payment charge. The correct structure for early retirement is to build the ISA alongside the SIPP during the accumulation phase, sized to cover the years between the early retirement date and age 57. A target retirement at 55 with £30,000 per year in living costs requires £60,000 minimum in the ISA bridge. A target retirement at 52 requires £150,000.

Does the 2027 pension IHT change make ISAs more attractive than SIPPs in the UK?

For contribution decisions, no. The 40% tax relief advantage on SIPP contributions is too large to forfeit, regardless of the IHT change. For estate planning decisions, the April 2027 change makes the ISA relatively more attractive compared to the post-2027 pension because both are now within the IHT estate. The ISA additionally provides tax-free withdrawals and flexible access. For investors who will accumulate more pension wealth than they can spend in retirement, the optimal response is not to stop contributing to the SIPP but to draw pension income strategically each year and redirect it into the ISA, gradually shifting the mix.

Sources and Further Reading

HMRC Pension Tax Relief Statistics 2024, gov.uk/government/statistics. ABI ISA and Savings Statistics 2024, abi.org.uk. FCA Retirement Outcomes Review 2018, fca.org.uk. IFS, Pension Tax Relief: Distributional Analysis and Reform Options, 2023, ifs.org.uk. Bennyhoff, D.C. and Kahlenberg, F. (2012), Advisor Alpha, Vanguard Research. HMRC Consultation: Inheritance Tax on Unused Pension Funds, August 2024, gov.uk. PLSA Retirement Living Standards 2024, plsa.co.uk.

About the Author

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. He is the founder of the Great Investments Programme at campaignforamillion.com.

Disclaimer: This article is for information and educational purposes only. It does not constitute financial guidance specific to your personal circumstances. Tax rules are correct as of April 2026 and are subject to change. Consult a qualified professional for guidance tailored to your situation.

Comments