The Self-Employed Pension Guide 2026: Why a SIPP Is Your Most Powerful Financial Tool

- Alpesh Patel

- Apr 13

- 3 min read

Updated: Apr 25

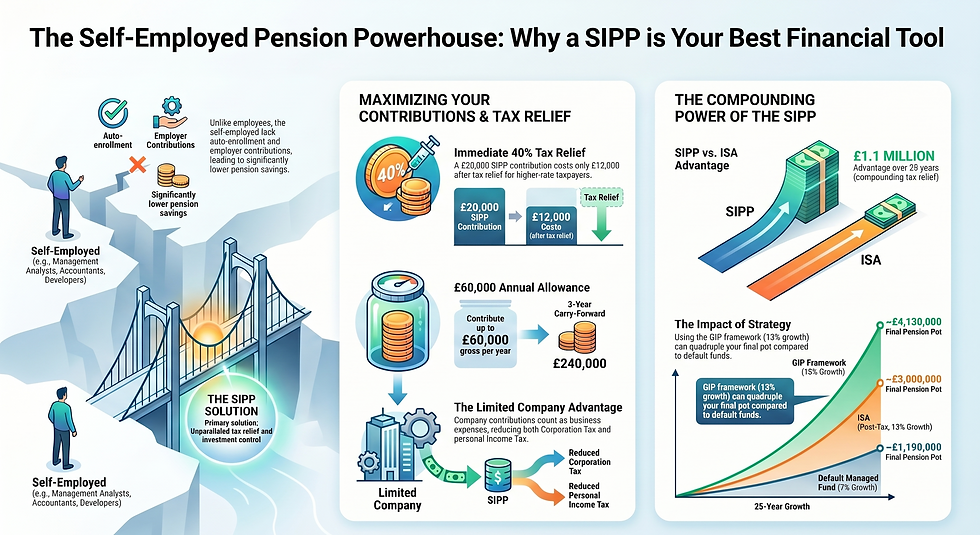

If you are self-employed, no one is building your pension for you. There is no employer contributing 3%, 5%, or 10% of your salary. There is no auto-enrolment quietly setting aside money every month. Your retirement provision is entirely the sum of the deliberate decisions you make or don’t make over your working life.

According to HMRC and DWP data, self-employed workers in the UK have significantly lower pension savings than employees at every age bracket. This is not primarily because self-employed people earn less many earn considerably more than the average employee. It is because the structure of auto-enrolment and employer contributions that quietly builds pension wealth for employees simply does not exist for the self-employed.

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. A significant proportion of GIP members are self-employed business owners, contractors, and consultants.

Why the SIPP Is the Self-Employed Investor’s Most Powerful Financial Tool

The Self-Invested Personal Pension (SIPP) is specifically designed for self-directed investors. You choose the platform. You select the investments. You control the contribution timing. And every pound you put in receives tax relief at your marginal rate making the SIPP the most efficient savings vehicle available to the self-employed.

For a self-employed person with £60,000 net profit, contributing £20,000 to a SIPP reduces their taxable income to £40,000. At 40% tax relief on the contribution, the real cost of the £20,000 SIPP contribution is £12,000 after tax. The £8,000 tax saving compounds inside the SIPP alongside the full £20,000 contribution. No other investment vehicle offers this kind of upfront guaranteed return.

How Much Can Self-Employed People Pay Into a SIPP?

Annual allowance: up to £60,000 gross per year (2026/27), or 100% of relevant UK earnings if lower. For sole traders, relevant earnings is net profit. For limited company directors, salary is the relevant earnings but the company can also make employer contributions directly into your SIPP.

Limited company directors: the company can make employer contributions directly to your SIPP as a business expense. These reduce your corporation tax bill as well as your personal income tax. A limited company director contributing £60,000 via employer contributions saves corporation tax at 25% on the contribution AND avoids income tax and National Insurance on that income.

Carry-forward: unused allowance from the previous three tax years can be carried forward and used in a single year, up to £240,000 gross (subject to earnings). For self-employed investors who have had variable income years, carry-forward is particularly valuable.

The Compounding Numbers: What Regular SIPP Contributions Become

A self-employed investor at 40 contributing £1,500/month gross (£900/month net after 40% tax relief) for 25 years:

At 7% (default managed fund): final pot approximately £1,190,000

At 13% (GIP framework): final pot approximately £4,130,000

The £900/month net cost to the investor (after 40% tax relief) produces £4.1 million over 25 years at 13% growth. The same £900/month invested outside a pension, with no tax relief, in an ISA at 13%, produces approximately £3.0 million. The SIPP advantage over the ISA, just from the upfront tax relief compounding over 25 years, is over £1.1 million.

The Three SIPP Platforms Best Suited to Self-Employed Investors

Fidelity: low FX rate (0.25%), low dealing commission (£1.50), good fund range. Best for active international stock-pickers making regular contributions.

Interactive Investor: flat monthly fee (£11.99/month). Best for larger SIPP pots (£50,000+) with infrequent trading. The flat fee advantage grows as the pot grows.

Trading 212: zero platform fee, zero dealing commission, 0.15% FX. Best for cost-focused self-directed investors making regular, smaller contributions across international stocks.

For a personalised self-employed pension assessment including contribution strategy, platform selection, and how the GIP framework applies to your SIPP - book a free portfolio review here

Sources & Further Reading

HMRC — Pension contributions for self-employed people: how much you can pay in and claim tax relief. gov.uk

ONS / DWP — Self-employed pension participation rates and retirement savings gap. ons.gov.uk

MoneyHelper — Pensions for self-employed people. moneyhelper.org.uk

Disclaimer: This article is for educational purposes only. Tax rules are subject to change. All projections are illustrative. This does not constitute personal financial or tax guidance. Always verify current rules with HMRC or a qualified professional.

Alpesh Patel OBE

Comments