Jeremy Grantham - Is He Wrong? Or Will There Be a Stock Market Crash?

- Alpesh Patel

- 3 days ago

- 5 min read

Updated: 1 day ago

In the pantheon of market bears, Jeremy Grantham sits on a throne built of prescient warnings and mistimed exits.

As a legendary "bubble spotter," his credentials are unimpeachable: he famously identified the Japanese asset bubble, the dot-com collapse, and the U.S. housing crisis long before the first cracks appeared in the foundation. To many, he is the ultimate sage of financial excess.

Yet, a troubling paradox haunts those who follow his lead. While Grantham’s intellectual rigour is undeniable, adhering to his bearish proclamations has often resulted in staggering financial loss for the average investor.

This raises a fundamental question for the modern portfolio: why does following a brilliant mind so often lead to a depleted brokerage account? The answer lies in the chasm between being intellectually correct and being investment-useful.

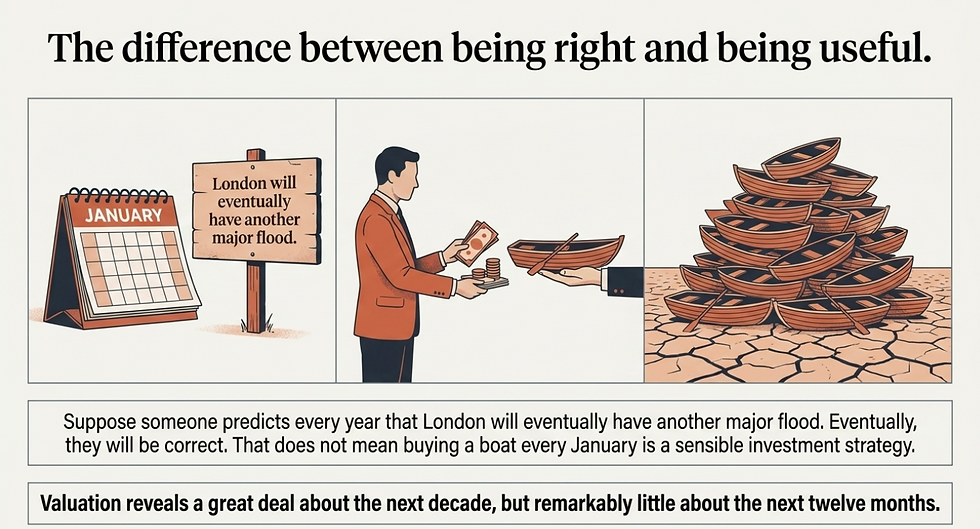

Stock Market Valuation Is Not Market Timing: The "London Flood" Problem

Identifying a bubble and generating returns are not just different skills—they can be mutually exclusive. To understand the "Prophet’s Paradox," consider the "London flood" analogy.

If a resident of London predicts every January that the city will eventually suffer a catastrophic flood, they will, given enough time, be proven right. However, that eventual correctness does not make the purchase of a lifeboat every single winter a sensible investment strategy.

The central weakness of a purely valuation-based philosophy is that it attempts to use a long-term compass for a short-term journey. Valuation tells us a great deal about what the next decade might look like, but it tells us remarkably little about the next twelve months.

Stock markets do not simply hit "fair value" and mean-revert; they have a terrifying capacity to move from expensive to very expensive, then to absurdly expensive, and finally to levels that defy all historical logic.

"The investor who exits too early receives no prize for intellectual correctness."

In the theater of the markets, being the first person to smell smoke is only profitable if the rest of the audience doesn't decide to stay and watch the show for another five years.

Why Today's Stock Market Tech Giants Aren't Pets.com

A primary mistake of the "permanent bear" is the reductionist assumption that all bubbles are identical. When the modern bear looks at the current market, they see the ghost of 1999- thousands of businesses with no revenue and no sustainable profits. But this template is an unreliable guide for the current era.

Today’s market leaders, such as Microsoft, Nvidia, Alphabet, Meta, and Amazon, are fundamentally different animals than the speculative shells of the dot-com era like Pets.com.

While the bears view the current Artificial Intelligence boom as a mere sequel to the 1999 circus, they overlook a critical shift: extraordinary earnings growth. Today’s tech titans are not just selling dreams; they are generating tens of billions of dollars in annual free cash flow, dominating global markets with immense pricing power, and owning the digital infrastructure that competitors find nearly impossible to replicate.

As the source context notes, this growth continually changes the very definition of "fair value" in real-time. A company that looks expensive today may actually be fairly priced relative to the earnings it will generate tomorrow. Assuming these profit engines are worthless speculative vehicles is the trap that keeps many investors on the sidelines while wealth is being created.

The Psychology of the Stock Market Perma-Bear

Behavioural finance suggests that even the most brilliant minds can become victims of their own expertise. For an investor like Grantham, being "the bubble guy" isn't just a strategy; it's an identity. Once this framework is established, several psychological traps snap shut:

Identity: When your reputation is built on spotting disasters, optimism feels like an act of betrayal. Changing course isn't just a portfolio adjustment; it’s a public abandonment of your life’s work.

Availability Bias: Humans expect the future to resemble the most memorable events of their past. If an investor's greatest successes came from identifying a crash, they view every period of market exuberance through that specific, traumatic lens.

Confirmation Bias: Once a bearish framework is adopted, the brain becomes a heat-seeking missile for bad news. Evidence of a crash is magnified, while evidence of innovation or earnings growth is dismissed as "irrationality."

Asymmetric Incentives: There is a unique "reputational payoff" to being a bear. If the crash never happens, you are merely "early." If it eventually arrives, you are hailed as a prophet. This creates a low-risk environment for career bears to maintain a stance that is disastrous for their clients but beneficial for their brand.

The Dangerous Allure of Unfalsifiable Logic in The Stock Market

The most seductive trap of the permanent bear is the creation of an unfalsifiable worldview. For the human brain, this is a comfort mechanism; for the portfolio, it is a poison.

In this framework, every market move is interpreted as a confirmation of the original thesis. If markets rise, the bubble is simply getting bigger and the eventual "reckoning" more severe. If they fall, the crash has begun. If valuations widen, it’s "irrational exuberance." If they narrow, the top is in.

This is the "Identity Trap" in action. The brain treats a rising market not as a signal that the thesis is wrong, but as an insult to the investor's intelligence. By dismissing the market’s gains as "irrational," the bear preserves their ego while losing their capital.

A truly scientific approach to investing requires testing ideas that can be proven wrong. A worldview that can never be disproved is not a strategy—it’s a dogma.

The Invisible Killer in The Stock Market : Opportunity Cost

In the world of finance, a 50% crash is a headline-grabbing explosion. It is visible, painful, and visceral. However, opportunity cost is the invisible killer, and over a lifetime, it is often far more lethal to wealth.

The mathematics of compounding are brutal and unforgiving. A portfolio compounding at 12% annually doubles roughly every six years. If an investor sits out just one decade while waiting for an "inevitable" crash that takes its time arriving, they don't just lose ten years of returns; they miss nearly two full "doubling cycles" of their entire net worth.

The "cost" of being safely on the sidelines can eventually exceed the damage of the very crash the investor was trying to avoid.

"In investing, being early is often indistinguishable from being wrong."

Conclusion: Finding the Middle Ground in The Stock Market

Jeremy Grantham should be respected as a master student of financial excess, but his worldview is a warning, not a roadmap. The balanced takeaway is to respect his study of price and valuation without allowing it to paralyze your participation in the engine of wealth creation.

While price always matters, it must be weighed against the reality of innovation, the momentum of earnings growth, and the historical fact that markets can stay irrational longer than you can stay solvent. Ultimately, identifying excess is only half of the job.

The other half is understanding how long that excess can persist and how costly permanent pessimism can become.

As you look at your own portfolio, you must ask the difficult question: Are you managing your money to satisfy your ego and be "intellectually correct" about a future disaster, or are you managing it to fund your future?

In the long run, the power of compounding usually offers a much larger prize than the satisfaction of being the first one to call the top.

Disclaimer: The views expressed in this article are for informational and educational purposes only and do not constitute financial, investment, legal, or tax advice.

References to Jeremy Grantham, market valuations, technology companies, or historical investment outcomes are intended for commentary and analysis and should not be interpreted as recommendations to buy, sell, or hold any security.

Past performance is not indicative of future results, and all investments involve risk, including the potential loss of principal. Market conditions, valuations, and economic circumstances can change rapidly, and opinions expressed herein may evolve over time.

Readers should conduct their own research and consult a qualified financial professional before making any investment decisions.

Alpesh Patel OBE

Comments