UK Pension Annual Allowance 2026/27: How to Maximise Your Contributions

- Alpesh Patel

- Apr 13

- 3 min read

Updated: Apr 20

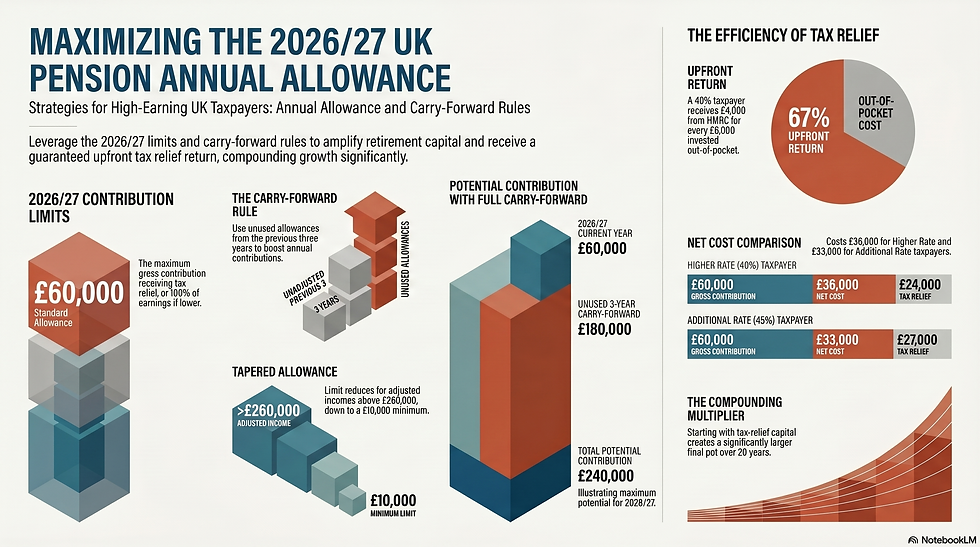

The pension annual allowance is the single most underused tax break available to UK investors. A 40% taxpayer contributing £10,000 gross to their SIPP pays £6,000 out of pocket and receives £4,000 from HMRC. There is no other investment with a guaranteed 67% upfront return on the capital you put in.

For 2026/27, the standard annual allowance is £60,000 (or 100% of earnings if lower). The carry-forward rule means you can bring forward unused allowance from the previous three tax years, potentially enabling a single-year contribution of up to £180,000. For high earners, the tapered annual allowance reduces the standard allowance if adjusted income exceeds £260,000.

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. Maximising the annual allowance is the first step discussed in every GIP portfolio review.

The 2026/27 Annual Allowance: The Key Numbers

Standard annual allowance: £60,000 (or 100% of earnings, whichever is lower). This is the maximum gross pension contribution that receives tax relief in the 2026/27 tax year. Both your own contributions and employer contributions count toward this limit.

Money Purchase Annual Allowance (MPAA): £10,000 triggered if you have started drawing flexible income from a defined contribution pension. Carry-forward cannot be used to exceed the MPAA.

Tapered annual allowance: For adjusted income above £260,000, the annual allowance reduces by £1 for every £2 of excess income, down to a minimum of £10,000. Threshold income (income excluding pension contributions) must also exceed £200,000 for the taper to apply.

Lifetime allowance: Abolished from April 2024. There is no longer a cap on the total amount you can hold in a pension without charge - only the annual allowance limits how much you can contribute in any given year.

Carry-Forward: How to Contribute Up to £180,000 in a Single Year To UK Pension

Carry-forward allows you to use unused annual allowance from the previous three tax years. To use carry-forward, you must have been a member of a registered pension scheme in the year you are carrying forward from, even if you made no contributions in that year. You also need sufficient earnings in the current year to cover the total contribution.

Practical example: If you contributed nothing in 2023/24, 2024/25, and 2025/26 (allowances of £60,000, £60,000, and £60,000), you could carry forward £180,000 of unused allowance and add it to the £60,000 current year allowance - enabling a maximum single-year gross contribution of £240,000, subject to earnings. For a business owner who has had a strong year or is approaching a business sale, this is an extraordinarily powerful tax planning tool.

The Tax Relief Calculation: What It Actually Costs You

Basic rate taxpayers receive 20% tax relief. The pension scheme claims this automatically from HMRC - you pay £800, the SIPP receives £1,000. Higher rate taxpayers can claim an additional 20% through Self Assessment, bringing the effective cost of £1,000 gross contribution to £600. Additional rate (45%) taxpayers can claim a further 5%, bringing the effective cost to £550 per £1,000 gross.

Basic rate (20%): £60,000 gross contribution costs £48,000 net. HMRC adds £12,000.

Higher rate (40%): £60,000 gross contribution costs £36,000 net after basic and higher rate relief. HMRC adds £24,000 total.

Additional rate (45%): £60,000 gross contribution costs £33,000 net. HMRC adds £27,000 total.

The Compounding Multiplier: Why the Tax Relief Compounds Too

The 40% tax relief is not just a one-off saving on the contribution. It means you are starting your compounding journey with 67% more capital than you paid for. A 40% taxpayer who contributes £60,000 net over 10 years has £100,000 working in their SIPP rather than £60,000 - a difference that, at 13% GIP framework growth, is worth approximately £338,000 in additional final pot value after 20 years.

For a calculation of your own annual allowance position, carry-forward availability, and how maximising contributions to your SIPP interacts with the GIP framework, book a free portfolio review here

Sources & Further Reading

HMRC — Pension annual allowance, carry-forward rules, and tapered allowance guidance. gov.uk/tax-on-your-private-pension/annual-allowance

MoneyHelper — Annual allowance for pension savings: limits, carry-forward, and tax charges. moneyhelper.org.uk

Financial Times — Pension annual allowance, tax relief, and high earner planning. ft.com/personal-finance

Disclaimer: This article is for educational purposes only. Tax rules are subject to change. This does not constitute personal tax or financial guidance. Always verify current allowances with HMRC or a qualified tax professional before making contributions.

Alpesh Patel OBE

Comments