There Is Never a Moment That Feels Right to Invest: The Emotional Cycle of the Market-Timing Mind

- Alpesh Patel

- Apr 18

- 6 min read

Updated: Apr 27

There is no market condition that produces the feeling of the right moment to invest. This is not because market conditions are always bad. It is because the feeling of readiness that investors are waiting for is generated by psychological mechanisms that are, by their nature, never satisfied. The cycle - from ‘calm, maybe wait for a dip’ through ‘too scary’ to ‘back to all-time highs, told you it was expensive’ was first described by psychologist Kurt Lewin in 1935 as approach-avoidance conflict. It does not resolve with time. It intensifies.

Alpesh Patel OBE is a hedge fund manager, Bloomberg TV alumnus, Financial Times author, and former Visiting Fellow at Corpus Christi College, Oxford. Approach-avoidance conflict is among the most common presentations in GIP investor consultations — and the six-stage cycle described in this post maps almost exactly onto what investors describe when asked why they have not yet acted.

Kurt Lewin and Approach-Avoidance Conflict

Kurt Lewin was a Prussian-born social psychologist whose 1935 work A Dynamic Theory of Personality introduced the concept of psychological field theory and, specifically, approach-avoidance conflict: a state in which a single goal simultaneously generates both an approach motivation (the desire to obtain it) and an avoidance motivation (the desire to avoid the discomfort associated with obtaining it). Lewin’s critical finding was that avoidance motivation grows stronger as the individual gets closer to the goal. The nearer the decision to invest, the stronger the avoidance response becomes. This is why investors can discuss investing calmly in the abstract but feel acute anxiety when the cursor is hovering over the confirm button.

Neal Miller at Yale confirmed and extended Lewin’s framework in 1944, establishing that the conflict state self-reinforces: the longer it persists, the more entrenched both the approach and avoidance motivations become, and the more psychologically difficult it is to break. An investor who has been in approach-avoidance conflict for 12 months faces a harder psychological task than one who has been in it for 12 days not because the market has changed, but because the conflict has deepened.

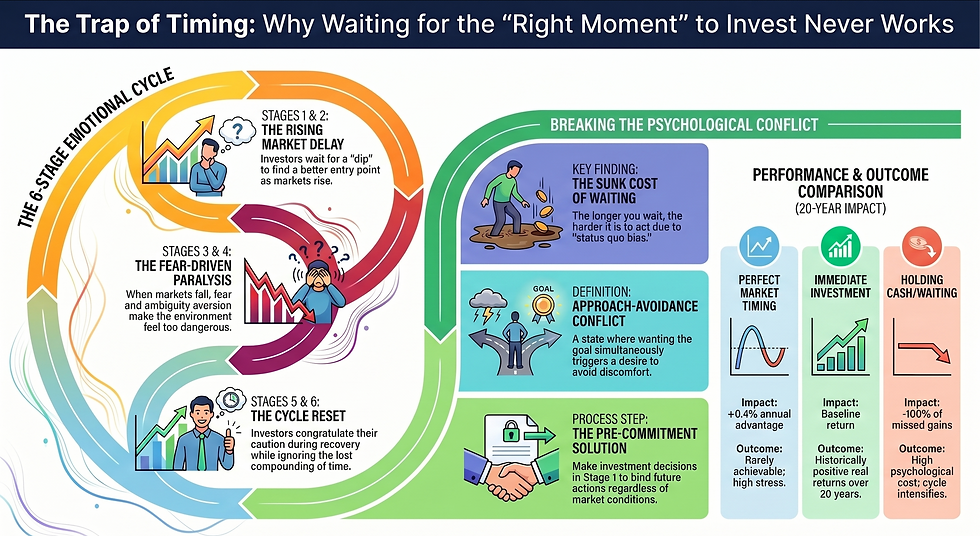

The Six-Stage Cycle: Every Market Condition Generates a New Reason to Wait

Stage 1 - Market is calm: The approach motivation is active. But the avoidance motivation generates a counter-narrative: the market has been rising, a correction must be coming, waiting for a dip will produce a better entry. The investor delays.

Stage 2 - Market rises 5%: Loss aversion activates around the foregone gain. New narrative: a correction is now more likely given the rise, wait for a pullback. The investor delays.

Stage 3 - Market falls 5%: The correction arrived but it feels dangerous. New narrative: this could go further, wait for it to stabilise. Loss aversion makes the falling market feel threatening rather than opportunistic. The investor delays.

Stage 4 - Market falls 10%: Cortisol is elevated. The amygdala is dominating the prefrontal cortex. Ambiguity aversion — the preference for known risk over unknown risk documented in Daniel Ellsberg’s 1961 paradox is fully active. New narrative: this is a crash, wait for clarity. The investor delays.

Stage 5 - Market recovers partially: The investor is now psychologically invested in having waited. Acting now means admitting the wait was pointless. Status quo bias reinforces inaction. New narrative: too uncertain, could reverse again. The investor delays.

Stage 6 - Market returns to all-time high: Stage 1 logic re-asserts. The investor congratulates themselves for their caution without calculating 12 to 18 months of compounding missed. The cycle resets.

The Sunk Cost of Waiting: Why Longer Delays Become Harder to Break

Richard Thaler’s endowment effect, the finding that people value things more once they own them and resist departing from their current state simply because they have held it - applies directly to the waiting investor. After three months of waiting, investing means giving up three months of careful deliberation. After six months, it means abandoning a considered strategy. After 12 months, it means conceding that 12 months of caution was a mistake. The psychological cost of acting grows in proportion to the duration of waiting, independently of any market movement. This is why the cycle intensifies over time and why Peter, in the Schwab study, so rarely finds the right moment: each passing month makes the right moment require not just a market condition but a psychological permission that becomes increasingly costly to grant.

Breaking the Cycle: Pre-Commitment at Stage One

Lewin’s own research and Miller’s 1944 extension established that the only reliable exit from approach-avoidance conflict is a structural change to the decision environment — not a change in motivation. The relevant structural change is pre-commitment: making the investment decision in Stage 1 (when avoidance motivation is at its lowest) and binding it to execute on a specified future date regardless of market conditions. Thaler and Benartzi’s Save More Tomorrow research (Journal of Political Economy, 2004) demonstrated that pre-commitment to future action is significantly more effective than relying on willpower at the moment of decision. The cycle can only be broken at Stage 1. By Stage 4, the avoidance motivation is too strong and the psychological investment in waiting too deep.

Frequently Asked Questions

Is now a good time to invest in the UK stock market 2026?

The question itself is the trap. Schwab (2012) established that perfect timing across 20 years produces only a 0.4% annual advantage over immediate investment. Siegel’s Stocks for the Long Run shows every rolling 20-year period in developed market history produced positive real equity returns. For a long-term investor with a systematic framework and a three-plus-year holding horizon, the question of whether now is a good time is less relevant than whether the businesses being purchased pass the GIP quality screens. The best time to invest is when you have the capital, the framework, and a defined entry plan.

Why do I always find a reason not to invest?

This is approach-avoidance conflict described by Kurt Lewin in 1935. The investor simultaneously wants to invest (approach motivation) and wants to avoid the discomfort of investing (avoidance motivation). Every market condition generates a new reason for the avoidance motivation to prevail — not because conditions are genuinely risky, but because the avoidance motivation responds to the proximity of a feared outcome, not to market facts. The reasons change as conditions change; the underlying refusal remains constant.

What is approach-avoidance conflict in investing?

Approach-avoidance conflict is a motivational psychology concept described by Kurt Lewin (1935) and extended by Neal Miller at Yale (1944). It describes a state where a single goal generates both motivation to pursue it and motivation to avoid the discomfort of pursuing it. Applied to investing: the goal of owning a well-selected portfolio generates approach motivation (wanting the returns) and avoidance motivation (fear of loss, timing anxiety). The conflict does not resolve through waiting — both motivations persist, and the avoidance motivation strengthens as the decision approaches.

Should I wait for a market crash before investing UK 2026?

No. Waiting for a crash requires predicting both when it occurs and when it has ended — a double prediction that professional fund managers consistently fail to make (SPIVA 2024: 87% of active UK managers underperform their benchmark over 10 years). Historical data shows that even investors who buy at the absolute market peak — as Bad Bart did in the Schwab study — outperform investors who hold cash waiting for better conditions. The cost of being out of the market during a rally consistently exceeds the cost of buying before a fall.

What is the endowment effect and how does it affect investment decisions?

The endowment effect, documented by Richard Thaler and incorporated into Kahneman’s behavioural economics framework, describes the finding that people value things more once they own them and resist departing from their current state because they have held it. Applied to the waiting investor, the cash position becomes psychologically valued simply by virtue of being the current state. The longer cash has been held, the higher its psychological value — and the higher the perceived cost of moving into investments. This is why waiting longer makes it harder, not easier, to act.

How do I stop waiting and start investing?

The most reliable method, supported by Thaler and Benartzi’s pre-commitment research (Journal of Political Economy, 2004), is to make the decision now and bind it to a specific future execution date rather than relying on willpower at the moment of entry. Write down the amount you will invest, the date within the next 14 days on which you will invest it, and the five positions across which you will divide it equally. This transfers the decision from your future anxious self — who may be in Stage 3 or Stage 4 of the emotional cycle — to your current calm self. The execution then becomes mechanical, not emotional.

To break the cycle with a structured first-entry plan and the GIP Approved List, book a free GIP portfolio review here

Academic Sources & Further Reading

Lewin, K. (1935). A Dynamic Theory of Personality. McGraw-Hill.

Miller, N.E. (1944). Experimental studies of conflict. In J. McV. Hunt (Ed.), Personality and the behavior disorders. Ronald Press.

Thaler, R. & Benartzi, S. (2004). Save More Tomorrow. Journal of Political Economy, 112(S1), S164–S187.

Kahneman, D. & Tversky, A. (1979). Prospect Theory. Econometrica, 47(2), 263–291.

Samuelson, W. & Zeckhauser, R. (1988). Status Quo Bias in Decision Making. Journal of Risk and Uncertainty, 1(1), 7–59.

Ellsberg, D. (1961). Risk, Ambiguity, and the Savage Axioms. Quarterly Journal of Economics, 75(4), 643–669.

Disclaimer: This article is for educational purposes only. All investing carries risk. This does not constitute personal financial guidance.

Alpesh Patel OBE | www.campaignforamillion.com

Comments